KARACHI: Pakistan has decided to impose regulatory duty at 10 per cent from July 01, 2022.

The country presented its federal budget 2022/2023 on June 10, 2022 and proposed increase on regulatory duty on various imported goods.

READ MORE: Penalty amount revised for late filing income tax returns

The Finance Bill, 2022 suggested levying 10 per cent regulatory duty on import of motor spirit as against existing rate of zero percent.

Experts at PwC A.F. Ferguson Chartered Accountants said that the notifications for amendments relating to regulatory duty and additional duty are yet to be issued. “The comments are based on ‘Salient Features’ issued with the finance bill,” they added.

READ MORE: Advance tax on immovable property purchase enhanced to 250% for non-filers

The government also proposed increase in regulatory duty from zero per cent to 10 per cent on other paper, paperboard, cellulose wadding and webs of cellulose fibers.

Furthermore, the government planned to increase regulatory duty from 10 per cent to 20 per cent on optic fiber cables.

The Finance Bill also proposed amendments in reduction of regulatory duties, which included:

Regulatory duty has been proposed to be reduced as follows:

Case hardening steel from 30 per cent to 20 per cent

Chrome yellow from 15 per cent to 0 per cent

The Finance Bill proposed reduction / concessions in customs duty:

Customs Duty (CD) leviable on the import of following categories of items / sectors is proposed to be exempted for incentivizing the respective sectors:

READ MORE: Pakistan massively increases taxation on motor vehicles

– Machinery and capital goods for mechanization of farming including machinery pertaining to irrigation, drainage, harvesting, plant protection etc.

– Specified raw materials used for manufacturing of LED lights, LED bulbs (including parts thereof) and brush ware.

– 26 Active Pharmaceutical Ingredients for incentivizing Pharmaceutical manufacturers.

– Raw materials for manufacture of first aid bandages.

– Membranes for filtering / purifying water.

– The drug ‘Grafalon’ and gadget ‘Irisvision’.

– Raw materials of Ivy leaves extract powders.

– Motor spirit.

In addition to CD, Additional Customs Duty (ACD) is also proposed to be exempted on import of the following goods:

– Raw materials imported by paper sizing industry and chlorinated paraffin wax industry and manufacturers of aluminum conductor composite cores.

– Stamping foils for manufacturing of optic fiber cables.

– Aluminum paste and powder imported by the Coating industry.

– Guts, bladders and stomachs of animals.

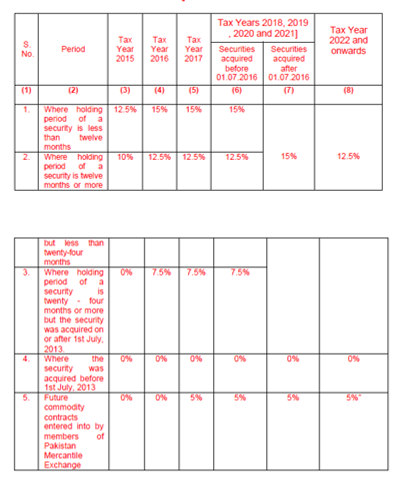

READ MORE: New rates of capital gain tax on disposal of securities

Reduction in Customs Duty and Additional Customs Duty

CD leviable on import of following goods is proposed to be reduced:

– Specified categories of other woven fabrics and artificial flowers / foliage of other materials imported by manufacturers of footwear.

– High-density fiber (HDF) boards of wood or other ligneous materials

– Specified fibers of polypropylene.

In addition to CD, ACD, leviable on import of following goods is also proposed to be reduced:

– Direct and reactive dyes.

– Glycerol crude and Glycerol for the coating industry.

– Goods pertaining to Aluminum, polymers of ethylene, Biaxially Oriented Polypropylene (BOPP) used by the packing industry.

– Adhesive, Epoxide resins, Filter media/ paper, Non-woven fabric media and Steel plates / sheets of prime quality imported by manufacturers of filters, other than automotive.

READ MORE: Pakistan slaps 45% corporate tax on banks

– Organic composite solvents and thinners imported by manufacturers of Dibutyl Orthophthalates.

– Plywood, veneered panels & similar laminated wood, poly (methyl methacrylate) and cyanoacrylate.

– Flavoring powders for food preparation for snacks manufacturers.