FBR, Pakistan’s national tax collecting agency, plays a crucial role in the country’s economy. Pakistan Revenue is committed to providing readers with the latest updates and developments regarding FBR activities.

ISLAMABAD: Federal Board of Revenue (FBR) has extended the date for payment and filing sales tax monthly return for the month of March 2020.

In a circular issued on Saturday, the FBR extended the last date for making payment of sales tax up to April 27, 2020, which was due on April 15, 2020.

Similarly, the FBR extended the last date for filing sales tax monthly return up to April 30, 2020, which was due on April 18, 2020.

The FBR facilitated the taxpayers in making sales tax payment and filing return due to lockdown to contain coronavirus.

The government extended the lockdown period up to April 30, 2020 in order to contain the outbreak of coronavirus pandemic.

KARACHI: A top official of Federal Board of Revenue (FBR) has informed the office bearers of Karachi Chamber of Commerce and Industry (KCCI) that a tax relief package for business community was under consideration in order to dilute the adverse impact of coronavirus pandemic (COVID-19).

ISLAMABAD: The collection of withholding tax from phone subscribers registered a phenomenal increase of 630 percent to Rs27 billion during first half of the current fiscal year, according to data made available to PkRevenue.com

The sources in Federal Board of Revenue (FBR) told that the restoration of withholding tax on phone usage by the Supreme Court of Pakistan (SBP) helped the tax authorities to generate substantial amount during the period under review.

The data revealed that the FBR collected withholding tax to the tune of Rs27 billion during first six months (July – December) 2019/2020 as compared with Rs3.7 billion collection in the corresponding period of the last fiscal year.

The FBR collects withholding tax on telephone usage under Section 236 of Income Tax Ordinance, 2001 from telephone subscribers and internet.

The tax rate is zero percent on monthly bill up to Rs1,000. However the bill exceeding Rs1,000 shall liable to tax rate at 10 percent.

In case subscriber of internet, mobile telephone and pre-paid internet or telephone card the tax rate shall be 12.5 percent of the amount of bill or sales price of internet pre-paid card or prepaid telephone card or sale of units through any electronic medium or whatever form.

The phone companies preparing bills or selling prepaid cards are responsible to collect withholding tax on behalf of the FBR from telephone subscribers, internet subscribers, purchaser of internet prepaid cards.

The withholding tax collected from phone usage is adjustable against the taxpayers’ liability.

The FBR incurred a loss of Rs55 billion in 2018/2019 due to suspension of withholding tax on telecommunication services by the Supreme Court of Pakistan.

In a continued effort to combat the COVID-19 pandemic, the Federal Board of Revenue (FBR) has issued an updated list of duty and tax-exempt items crucial for the prevention and control of the virus.

ISLAMABAD: Federal Board of Revenue (FBR) has exempted the withholding tax on commission agent for disbursement of Ehsaas Emergency Program.

The FBR issued SRO 315(I)/2020 dated April 16, 2020 to make amendment to Second Schedule of Income Tax Ordinance, 2001.

According to the amendment, a new clause 102A inserted to Part IV of the Second Schedule, which stated: “The provisions of Section 233 shall not apply to commission received by a retail branchless banking agent on any amount disbursed by the Ehsaas Emergency Cash Transfer Program for the period commencing on the date of issuance of this notification and ending on the 30th day of June, 2020.”

The Section 233 of the Income Tax Ordinance, 2001 explains application of withholding tax on brokerage and commission.

Where any payment on account of brokerage or commission is made by the Federal Government, a Provincial Government, a Local Government, a company or an association of persons constituted by, or under any law (hereinafter called the “principal”) to a person (hereinafter called the “agent”), the principal shall deduct advance tax at the rate specified in Division II of Part IV of the First Schedule from such payment.

If the agent retains Commission or brokerage from any amount remitted by him to the principal, he shall be deemed to have been paid the commission or brokerage by the principal and the principal shall collect advance tax from the agent.

KARACHI: Despite elimination of exemption and strengthening enforcement the duty free import surged by 17.1 percent during 2018/2019, according to official documents.

The FBR in its report released this month said that the duty free imports increased by 17.1 percent to Rs2,445 billion during fiscal year 2018/2019 as compared with Rs2,087 billion in the preceding fiscal year.

The documents revealed that goods under Chapter 27 of Customs Tariff were imported duty free worth Rs600 billion during fiscal year 2018/2019 as compared with Rs491 billion in the corresponding period of the preceding fiscal year.

The import of products including Mineral fuels, mineral oils and products under this chapter has increased by 22.3 percent during the period under review.

An amount of Rs317 billion has been allowed duty free for the import of boilers, machinery and mechanical during fiscal year 2018/2019, which is 12.5 percent higher than Rs282 billion in the same period of the preceding fiscal year.

The customs authorities granted duty free import of around Rs189 billion for the clearance of organic chemical during fiscal year 2018/2019 as compared with Rs144.85 billion in the preceding fiscal year, showing growth of 30.5 percent.

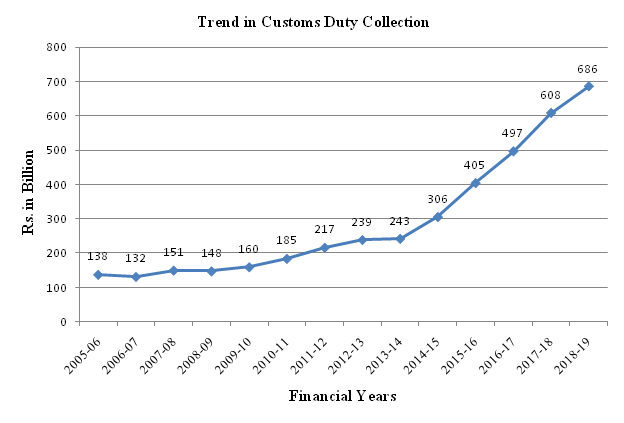

Despite lowering of tariff over the years, the customs duty is still one of the important sources of Federal Tax collection. The Dutiable Imports are the tax base for Customs Duty.

The collection of customs duty stood at around Rs686 billion and has contributed around 28.8 percent in the Indirect Taxes and 17.9 percent in total taxes during the F.Y.: 2018-2019.

It has increased by around 13 percent as compared to previous year.

The target of customs duty was Rs. 735 billion during FY: 2018-2019 which was missed by 6.7 percent.

Source: FBR

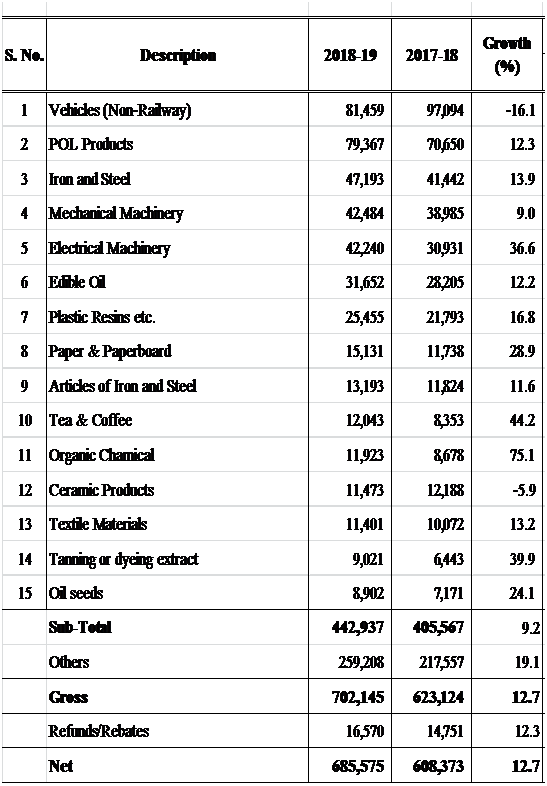

Out of 15 major revenue spinners, 13 items of imports recorded positive growth during FY: 2018-19 mainly due to increased Imports. On the other hand, only automobile (Ch:87) and ceramic products recorded negative growths.

The details of Customs Duty collection from major commodity groups (chapters) are presented in table below.

ISLAMABAD: The collection of withholding income tax from cash withdrawal from banks fell by 52 percent during first half of the current fiscal year as the government withdrew the levy on active taxpayers.

The collection of withholding income tax fell to Rs8.6 billion during July – December of current fiscal year 2019/2020 as compared with Rs17.8 billion collected in the corresponding period of the last fiscal year, according to official data.

Through Finance Act, 2019, the imposition of withholding tax on cash withdrawal by active taxpayers was eliminated in order to encourage income tax return filing.

However, the withholding tax rate at the rate of 0.6 percent is still leviable on persons not appearing on the active taxpayers list issued by the Federal Board of Revenue (FBR).

At present every banking company is required under Section 231A of Income Tax Ordinance, 2001 to collect withholding tax at 0.6 percent on payment for cash withdrawal, or sum total of payment for cash withdrawal, in a day, exceeding Rs50,000 for persons not appearing the Active Taxpayers List (ATL).

The same rate of 0.6 percent is applicable under Section 231AA and Section 231AA of the Ordinance on sale against cash of any instrument including demand draft, payment order, CDR, STDR, RTC, any other instrument of bearer nature or on receipt of cash on cancellation of any of these instruments where sum total of transactions exceeds Rs, 25,000 in a day, for persons not appearing in the Active Taxpayers’ List and transfer of any sum against cash through online transfer, telegraphic transfer mail transfer or any other mode of electronic transfer, where sum total of transactions exceed Rs. 25,000/-in a day, for persons not appearing in the Active Payers’ List.

ISLAMABAD: Tax collection from salary increase has sharply increased by 75 percent during first half (July – December) of current fiscal year 2019/2020 owing to changes brought in tax rates through Finance Act, 2019.

According to official data, the Federal Board of Revenue (FBR) collected Rs57.5 billion from salary income during July – December 2019/2020 as compared with Rs32.8 billion in the corresponding period of the last fiscal year.

It is pertinent to mention here that the threshold income has been enhanced to Rs600,000 for calculation of income tax for tax year 2020 as compared with Rs400,000 prevailed during tax year 2019.

The FBR issued withholding tax card for tax year 2019/2020 effective from July 01, 2019 under which every employer paying salary to employees above threshold income shall deduct withholding tax.

The FBR said that every person responsible for paying salary to an employee shall deduct tax from the amount paid under Section 149 of Income Tax Ordinance, 2001.

As per Finance Act, 2019, the provisions of newly inserted 10th schedule of the Income Tax Ordinance, 2001 shall not apply on tax deducted under section 149. Under the Tenth Schedule the withholding tax so collected shall be increased by 100 percent in case of persons not appearing on the Active Taxpayers List (ATL).

As per Finance Act, 2019, the salary slabs as well as tax rates have been revised with effect from 01.07.2019. As such all withholding tax agents disbursing salary are required to implement the revised tax rates from the same date.

Following are the salary slabs and rates on annual salary income:

TABLE

Salary Slabs

Tax Rates on salary slabs

1. Where taxable income does not exceed Rs. 600,000.

0 percent

2. Where taxable income exceeds Rs. 600,000 but does not exceed Rs. 1,200,000.

5% of the amount exceeding Rs. 600,000

3. Where taxable income exceeds Rs. 1,200,000 but does not exceed Rs. 1,800,000.

Rs. 30,000 plus 10% of the amount exceeding Rs. 1,200,000.

4. Where taxable income exceeds Rs. 1,800,000 but does not exceed Rs. 2,500,000.

Rs. 90,000 plus 15% of the amount exceeding Rs. 1,800,000

5. Where taxable income exceeds Rs. 2,500,000 but does not exceed Rs. 3,500,000

Rs. 195,000 plus 17.5% of the amount exceeding Rs. 2,500,000

6. Where taxable income exceeds Rs. 3,500,000 but does not exceed Rs. 5,000,000

Rs. 370,000 plus 20% of the amount exceeding Rs. 3,500,000

7. Where taxable income exceeds Rs. 5,000,000 but does not exceed Rs. 8,000,000

Rs. 670,000 plus 22.5% of the amount exceeding Rs. 5,000,000

8. Where taxable income exceeds Rs. 8,000,000 but does not exceed Rs. 12,000,000

Rs.1,345,000 plus 25% of the amount exceeding Rs. 8,000,000

9. Where taxable income exceeds Rs. 12,000,000 but does not exceed Rs.30,000,000

Rs. 2,345,000 plus 27.5% of the amount exceeding Rs. 12,000,000

10. Where taxable income exceeds Rs. 30,000,000 but does not exceed Rs.50,000,000

Rs. 7,295,000 plus 30% of the amount exceeding Rs. 30,000,000

11. Where taxable income exceeds Rs. 50,000,000 but does not exceed Rs.75,000,000

Rs. 13,295,000 plus 32.5% of the amount exceeding Rs. 50,000,000

12. Where taxable income exceeds Rs.75,000,000

Rs. 21,420,000 plus 35% of the amount exceeding Rs 75,000,000″;

The FBR said that every person responsible for making payment for directorship fee or fee for attending board meeting or such fee by whatever name called under Section 149(3) of Income Tax Ordinance, 2001 shall collect 20 percent of gross amount paid.

ISLAMABAD: Federal Board of Revenue (FBR) has released Rs51.5 billion sales tax refunds through fully automated online system since July 2020.

The FBR on Tuesday released information of release of refunds through Fully Automated Sales Tax E-Refund (FASTER) system.

As per record, since July 2019, a total of refunds amounting to Rs. 64.5 billion were claimed through FASTR System.

Out of it, refund cases of rupees Rs57 billion were processed. Out of these processed cases, refund payment of rupees 51.5 billion have been made to the exporters and businessmen so far.

The remaining unpaid refund cases have been withheld due to incomplete date provision by the exporters and businessmen.

The FBR introduced FASTER system for repayment of refunds to exporters against the deduction of taxes on their import of raw materials and other input taxes.

Through Finance Act, 2019 the sales tax zero rating was abolished for all the sectors availing the facility. However, in order to facilitate the exporters the FASTER system was introduced to make payment of their refunds within 72 hours.

FBR sources said that the tax authority had speed up the disbursement of refund payment to exporters, who were facing liquidity problems due to ongoing lockdown for prevention of coronavirus outbreak.

ISLAMABAD: Federal Board of Revenue (FBR) on Friday exempted income tax on donations made to Prime Minister’s Corona Relief Fund.

The FBR issued SRO 300(I)/2020 to make amendment to Second Schedule of Income Tax Ordinance, 2001 to allow exemption from whole of income tax on donations made to PM Corona Fund.

The FBR also granted exemption from minimum tax to the donations made towards the Prime Minister’s COVID-19 Pandemic Relief Fund – 2020.

The FBR also exempted the withholding tax deduction on non-cash banking transactions made by taxpayers not on the Active Taxpayers List (ATL) under Section 236P of the Income Tax Ordinance, 2001.

Further, Section 151, Section 231A and Section 231AA will also not apply to donations made to the Prime Minister Corona Relief Fund.