ISLAMABAD: The Pakistan Revenue Automation Pvt Limited (PRAL) has identified multiple vulnerabilities in Google Chrome, which are the most severe as those could allow for arbitrary code execution.

(more…)Tag: Federal Board of Revenue

The Federal Board of Revenue is Pakistan’s apex tax agency, overseeing tax collection and policies. Pakistan Revenue is committed to providing timely updates on the Federal Board of Revenue to its readers.

-

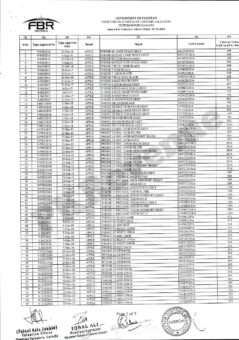

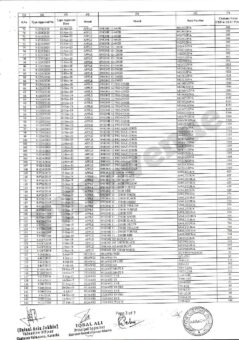

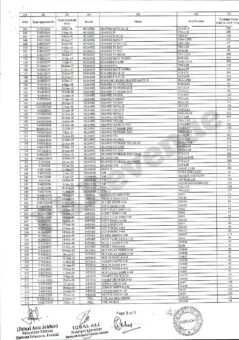

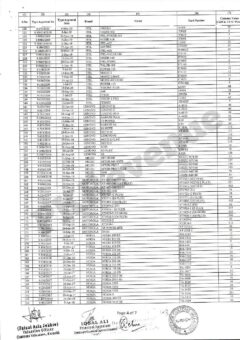

FBR issues fresh customs valuation for mobile phones

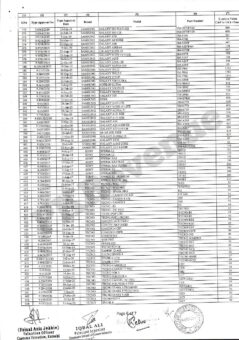

KARACHI: Federal Board of Revenue (FBR) has issued fresh customs values of mobile phone devices for the determination of duty and tax, sources said on Tuesday.

The Directorate General of Customs Valuation has issued valuation advice dated February 18, 2021, in respect of mobile phone devices to determine assessable customs values of mobile phone devices.

The directorate said that customs values as given in column 7 of the attached images may be considered for the purpose of assessment of duty and taxes.

These values will also be relevant for assessment and proceedings under SRO 1455(I)/2018 and SRO 1456(I)/2018 both dated November 29, 2018 read with Customs General Order No. 06/2018 dated November 29, 2018.

The directorate further said that the enclosed list is not exhaustive; however, mostly traded brands and models as provided by Mobile Phone Importers and Manufacturers Association (MPIMA).

For assessment of brands and models which are imported in commercial quantity but are not included in the enclosed annexure, the clearance collectorate have been advised to assess those under Section 81 of the Customs Act, 1969 and then forward a reference to the directorate for final determination of values thereof.

It further said that where in the enclosed annexure, type approval is not given or is under process, clearance collectorate shall fulfill the regulatory requirements pertaining for type approval/certificate of compliance from PTA first as envisaged under the law.

It is pertinent to mention that the valuation advice will be regularly updated and issued accordingly.

Following is the fresh customs valuation for mobile phone devices:

To watch the news in Urdu please visit and subscribe our YouTube Channel at

-

PTBA advises FBR stop interfering judicial function of Commissioner Appeals

ISLAMABAD: Pakistan Tax Bar Association (PTBA) has urged the Federal Board of Revenue (FBR) to stop interference in judicial function of Commissioner Appeals.

In a letter to FBR Chairman Muhammad Javed Ghani on Tuesday, the PTBA while referring to the instructions by the Legal Wing of the FBR to Commissioners Appeals, expressed serious concerns in interference in the judicial independence of the Appeal forum of the Commissioner Appeals and over the language of the letter which clearly indicates the direct influence in the judicial work/power of Commissioner Appeals.

The Legal Wing of the FBR in its letter directed the commissioner appeals that they may exercise powers under tax laws however unnecessary annulment of orders with directions may be avoided.

“Frequent annulled with directions orders will reflect adversely on the performance of the officers,” it added.

The PTBA said that the letter is a clear demonstration of the overt and covert pressure that is exerted on commissioner appeals by the FBR and the field officers.

“It is prima facie a travesty of justice in eyes of a taxpayer who is an aggrieved taxpayer is to seek relief from the departmental authorities which could be susceptible to overt and covert pressure from FBR.”

This letter of February 15, 2021 issued by the FBR Legal Wing clearly established direct interference of the FBR in judicial function of Commissioner Appeals. “This is just not acceptable to PTBA and its membership.”

An independent and fair appeal forum of the commissioner appeals is sine qua non for a taxpayer to have confidence in the tax administration.

The Supreme Court of Pakistan had elaborated this principle in a leading case by holding that ‘separation of judiciary from executive is the cornerstone of independence of judiciary.’

“If the taxpayer has confidence in a fair and just appeal forum of the FBR, he will come forward and be compliant taxpayer.

“An independent appeal forum of commissioner appeals free from influence and inference of the FBR and FBR field units will also reduce unethical practices prevalent in the field units.”

The PTBA demanded the FBR to withdraw the letter and re-assure all the commissioner appeals to adjudicate and decide appeals in a fair and just manner according to law and facts without any fear or influence from FBR or the FBR field units.

-

FBR allows income tax exemption on sugar import

ISLAMABAD: Federal Board of Revenue (FBR) on Tuesday allowed exemption from income tax on import of raw and refined sugar.

The FBR issued SRO 235(I)/2021 in pursuance to the federal cabinet decision dated January 26, 2021.

Through the SRO the FBR amended Second Schedule of the Income Tax Ordinance, 2001.

According to the amendments, the tax under Section 148 on commercial import of the white sugar shall be collected at the rate of 0.25 percent from January 26, 2021 till June 30, 2021.

Another clause added to the Second Schedule under which subject quota allotment by the commerce division, tax under section 148 shall be collected at the rate of 0.25 percent on import of raw sugar imported by sugar mills from January 26, 2021 to June 30, 2021 (both days inclusive) provided that such imports shall not exceed fifty thousand metric tons per sugar mill and three hundred thousand metric tons in aggregate by the sugar industry.

The FBR said that a new clause 12K had been inserted to the Second Schedule under which the provisions of Section 148 and Section 153 shall not apply on import and subsequent supply of five hundred thousand metric tons of white sugar imported by the Trading Corporation of Pakistan.

-

Concept of person defined for levy of income tax

Income Tax Ordinance, 2001 has defined the concept of person for the collection and deduction of tax on income.

The Income Tax Ordinance, 2001 updated up to June 30, 2020 issued by the Federal Board of Revenue (FBR), the “person” means a person as defined in section 80 of the Ordinance.

Section 80 defines person as:

(1) The following shall be treated as persons for the purposes of this Ordinance, namely: —

(a) An individual;

(b) a company or association of persons incorporated, formed, organised or established in Pakistan or elsewhere;

(c) the Federal Government, a foreign government, a political sub-Division of a foreign government, or public international organisation.

(2) For the purposes of this Ordinance —

(a) “association of persons” includes a firm, a Hindu undivided family, any artificial juridical person and anybody of persons formed under a foreign law, but does not include a company;

(b) “company” means —

(i) a company as defined in the Companies Ordinance, 1984 (XLVII of 1984);

(ii) a body corporate formed by or under any law in force in Pakistan;

(iii) a modaraba;

(iv) a body incorporated by or under the law of a country outside Pakistan relating to incorporation of companies;

(v) a co-operative society, a finance society or any other society;

(va) a non-profit organization;

(vb) a trust, an entity or a body of persons established or constituted by or under any law for the time being in force;

(vi) a foreign association, whether incorporated or not, which the Board has, by general or special order, declared to be a company for the purposes of this Ordinance;

(vii) a Provincial Government;

(viii) a Local Government in Pakistan; or

(ix) a Small Company as defined in section 2;

(c) “firm” means the relation between persons who have agreed to share the profits of a business carried on by all or any of them acting for all;

(d) “trust” means an obligation annexed to the ownership of property and arising out of the confidence reposed in and accepted by the owner, or declared and accepted by the owner for the benefit of another, or of another and the owner, and includes a unit trust; and

(e) “unit trust” means any trust under which beneficial interests are divided into units such that the entitlements of the beneficiaries to income or capital are determined by the number of units held.

-

What is permanent establishment under income tax law?

Income Tax Ordinance, 2001 has defined the meaning of permanent establishment of a foreign entity operating in Pakistan.

The Income Tax Ordinance, 2001 updated up to June 30, 2020 issued by the Federal Board of Revenue 9FBR), defined as “permanent establishment” in relation to a person, means a fixed place of business through which the business of the person is wholly or partly carried on, and includes –

(a) a place of management, branch, office, factory or workshop, premises for soliciting orders, warehouse, permanent sales exhibition or sales outlet, other than a liaison office except where the office engages in the negotiation of contracts (other than contracts of purchase);

(b) a mine, oil or gas well, quarry or any other place of extraction of natural resources;

(ba) an agricultural, pastoral or forestry property;

(c) a building site, a construction, assembly or installation project or supervisory activities connected with such site or project but only where such site, project and its connected supervisory activities continue for a period or periods aggregating more than ninety days within any twelve-months period;

(d) the furnishing of services, including consultancy services, by any person through employees or other personnel engaged by the person for such purpose;

(e) a person acting in Pakistan on behalf of the person (hereinafter referred to as the “agent”), other than an agent of independent status acting in the ordinary course of business as such, if the agent –

“(i) has and habitually exercises an authority to conclude contracts on behalf of the other person or habitually concludes contracts or habitually plays the principal role leading to the conclusion of contracts that are routinely concluded without material modification by the person and these contracts are─

(a) in the name of the person; or

(b) for the transfer of the ownership of or for the granting of the right to use property owned by that enterprise or that the enterprise has the right to use; or

(c) for the provision of services by that person; or”

(ii) has no such authority, but habitually maintains a stock-in-trade or other merchandise from which the agent regularly delivers goods or merchandise on behalf of the other person; or

Explanation.—For removal of doubt, it is clarified that an agent of independent status acting in the ordinary course of business does not include a person acting exclusively or almost exclusively on behalf of the person to which it is an associate; or ”;

(f) any substantial equipment installed, or other asset or property capable of activity giving rise to income;

(g) a fixed place of business that is used or maintained by a person if the person or an associate of a person carries on business at that place or at another place in Pakistan and─

(i) that place or other place constitutes a permanent establishment of the person or an associate of the person under this sub-clause; or

(ii) business carried on by the person or an associate of the person at the same place or at more than one place

constitute complementary functions that are part of a cohesive business operation.

Explanation.—For the removal of doubt, it is clarified that─

(A) the term ”cohesive business operation” includes an overall arrangement for the supply of goods, installation, construction, assembly, commission, guarantees or supervisory activities and all or principal activities are undertaken or performed either by the person or the associates of the person; and

(B) supply of goods include the goods imported in the name of the associate or any other person, whether or not the title to the goods passes outside Pakistan.

-

Income tax ordinance defines non-profit organization

Income Tax Ordinance, 2001 has defined the meaning of Non-Profit Organization for the purpose of tax treatment on the activity of NPOs.

The Income Tax Ordinance, 2001 up dated up to June 30, 2020 issued by the Federal Board of Revenue (FBR), explained as:

“Non-profit organization” means any person other than an individual, which is —

(a) established for religious, educational, charitable, welfare purposes for general public, or for the promotion of an amateur sport;

(b) formed and registered by or under any law as a non-profit organization;

(c) approved by the Commissioner for specified period, on an application made by such person in the prescribed form and manner, accompanied by the prescribed documents and, on requisition, such other documents as may be required by the Commissioner; and none of the assets of such person confers, or may confer, a private benefit to any other person.

-

Tax help desk at FPCCI to be set up after consultation: Javed Ghani

KARACHI: Muhammad Javed Ghani, Chairman, Federal Board of Revenue (FBR) on Monday said that a help desk to resolve tax problems of business community will be established at the apex trade body after consultation with FBR wings.

He was replying to various issues highlighted by members of Federation of Pakistan Chambers of Commerce and Industry (FPCCI) during his visit at the Federation House.

Muhammad Javed Ghani said that he has noted the matters at large given by the members of the trade bodies and said the FBR Help Desk will be established in FPCCI. “However, it requires consultation with various wings of FBR in order to open the desk for productive outcome.”

He further informed that the reduced human interactions is our policy towards which we are working and even we have improved the recent refunds in less period than it was earlier, which nearly is 70 to 80 percent more than the preceding period.

He also said that frequent and purposeful interaction with FPCCI is being recognized to be a good move in the objective development of the economy of the country.

Mian Nasser Hyatt Magoo, President, FPCCI said that it is high time to have paradigm shift in the tax structure to induce investment, promote production and grow economy instead of present revenucracy which remains the focus of FBR.

He said that constitutional and lawful position given to FPCCI through Act of parliament to represent the private sector of trade, industry and services which has been diluted by FBR through marginalized interaction with apex body.

He added that hardly any response is given by FBR against matters of members of trade bodies referred to FBR.

He further stated that the revenue generating agents are being ignored by FBR, which is against the obligation which it owns.

President FPCCI said that instead of negotiating with institutional representatives of FPCCI, FBR is attending Para shooters who have no locus standii to represent private sector stakeholders.

He said that FBR should not accord market practicing tax lawyers and tax consultants to represent FPCCI in the FBR various committees.

Mian Nasser Hyatt Maggo, President FPCCI said that FBR must come back to its past position since decade to negotiate trade, industry and business matters with/through apex body.

The FPCCI collects fiscal improvement proposals from all the members’ bodies of trade and industry and CCIs to consider the paradigm changes in the present taxation for promoting economy with incremental tax revenue on sustainable basis.

The apex body and its working on financial and other issues, if are taken up seriously with higher percentage of acceptance with higher level of seriousness of FBR would be a possible solution to make the budget which conduct business in harmony instead of amongst present conflicts and contradiction.

The attention of the FBR was invited towards present leverage to groups other than FPCCI, which is against the lawful representation which FPCCI enjoys.

It was said that the SMEs being said to be backbone of economy is being practically ignored and the persons of powerful and in-person connected groups have replaced the representation in decision making at FBR level.

The members from different trade bodies invited attention of FBR towards CNIC condition on sale which is counterproductive to required sales tax collection as well as impede the industrial production and markets sales.

Nowhere in the world CNIC or identity is asked from buyers, Pakistan is the only example set by FBR causing problems in business, in specific promoting the agitations on street by the agents of sales of produce, the conducting of small business be settled in peace by removing by removing CNIC condition for buyers.

The participants invited the attention of Chairman FBR that still the entry of raw materials in part II of 12th schedule of Section 148 of ITO has not been facilitated, which is in the exclusive domain of FBR to resolve.

The attention was also invited towards glaring example of not entering raw materials and sub-component imported by vendors under SRO 655 but on the contrary all the component imported by assemblers have been assigned part II of the 12th Schedule of Section 148.

This high handedness that weaker and SMEs segment not being well connected in the FBR committees are not being accommodated for otherwise on high reasonable ground.

Other manufacturers also claimed continued ignorance of their requests pending with FBR with zero response.

Tax structure on import of tea requiring rationalization was also put to the notice of Chairman FBR. Notices have become multiplied after the split of IRS commissionrates from earlier single unit to changed multiple units has eroded the concept of facilitation through One-Window.

The same showcase notice is now originating from various windows opened in IRS. The attention of Chairman FBR was also invited by the FPCCI towards the requirement of independence of tax judicial system, which presently negates the constitution and is pending since long for implementation in order to be constitutional compliant.

-

Pakistan Customs impounds non-duty paid vehicles worth Rs11.3 billion

ISLAMABAD: Pakistan Customs has impounded non-duty paid motor vehicles worth Rs11.3 billion during first seven months (July – January) of the current fiscal year, said a spokesman of the Federal Board of Revenue (FBR) on Sunday.

The seizure of non-duty paid motor vehicles registered growth around 66 percent as the customs authorities seized motor vehicles worth Rs6.8 billion in the same period of the last fiscal year.

The customs authorities confiscated smuggled goods worth Rs35 billion during the first seven months of the current fiscal year, showing an increase of 59 percent when compared with Rs22 billion in the corresponding months of the last fiscal year. It is pertinent to mention that the total seizures during the last fiscal year was Rs36 billion.

Giving the details of the seizure, the spokesman said that the customs authorities seized smuggled betel nuts amounting Rs3.4 billion during July – January 2020/2021, which was 105 percent higher than the seizer of in the same period of the last fiscal year.

A growth of 28 percent has been recorded in seizure of smuggled clothes and 70 percent rise recorded in illicit cigarettes.

The customs authorities confiscated auto parts worth Rs492 million, recording 113 percent growth than the last fiscal year.

Pakistan Customs seized high speed diesel worth Rs899 million and jewellery worth Rs271 million during the period under review.

The spokesman added that in its ongoing crackdown against sales of smuggled petroleum products through illegal fuel stations, the customs authorities sealed around 2000 petrol pumps.

-

Procedure issued for intimating retirement, submission of pension papers

ISLAMABAD: Federal Board of Revenue (FBR) has issued procedure for officers and staff of tax machinery regarding intimation about their superannuation retirement and submission of pension papers.

In supersession to Board’s earlier SOPs No. 25(20)MIR-IV/2016 dated 10.12.2020, the FBR said that while submitting the cases of retirement, pension papers and encashment of LPR for officers of field formations, the following documents must be attached with the application:-

I. RETIREMENT NOTIFICATION:

i. Application of the officer along with attested copies of CNIC and payslip

ii. Service Book & Matriculation Certificate (in original)

iii. Prescribed certificate regarding disciplinary and criminal proceedings (in original) format enclosed.

iv. Even if an officer does not submit application to the head of field formation for issuance of his/her retirement notification, it shall be incumbent upon the respective head to submit documents to the Board for issuance of retirement notification at least 3 months prior to his/her superannuation.

II. PREMATURE/ VOLUNTARY RETIREMENT:

The option for pre-mature/voluntary retirement after rendering 25 years of qualifying service shall be submitted along with all requisite documents mentioned above at least 06 months before the date of voluntary retirement with specific recommendations of the concerned Head of the field formation.

III. PENSION CASES:

i. Each page of pension papers must be signed and stamped (by name) by the DDO/Account Officer concerned and countersigned by the respective Head of office i.e. Chief Commissioner/ Chief Collector/ Director General/ Commissioner/ Collector/ Director.

ii. Pension application along with three attested Photographs.

iii. LPC (in original) issued by concerned AGPR/sub-offices of AGPR or District Accounts Officer (as the case may be).

iv. CNIC of the pensioner.

v. Prescribed certificate regarding disciplinary and criminal proceedings (format enclosed).

vi. No column of the pension papers should be left blank. Even if it is NIL, the same may be incorporated. Any irrelevant or inapplicable columns should be struck down.

(vii) While forwarding the pension papers, the respective Chief Commissioner/ Chief Collector/ Director General/ Commissioner/ Collector/ Director shall invariably submit recommendations about the release of full pension on the basis of satisfactory service of the pensioner or to withhold any portion of pension recording reasons thereof with evidences, in the relevant column, for decision by the Sanctioning Authority.

IV. LEAVE ENCASHMENT/LPR:

i. Leave admissibility certificate duly signed and stamped by the concerned officer of AGPR/ Sub-Offices of AGPR/District Account Officer

ii. In case of leave encashment, a certificate stating that the officer has not availed any kind of leave (except casual leave) during the last year of his/her service. In case leave is availed during last year, the details of leave availed, its nature and period with dates are to be specifically mentioned.

iii. Attested copy of retirement notification issued by the Board.

The FBR said that in case an application is not received with complete documentation, it will be returned with a copy of SOP indicating missing documents.