A signing ceremony between NBP and Waves was held in Lahore. With a commitment of Rs1.5 billion, NBP will be one of the largest financiers of the project.

NBP is also the mandated lead advisor and arranger for the upcoming syndicated finance facility to further develop the project.

This financing represents the active role NBP is playing to support the development of real estate sector in Pakistan.

Waves has been prominent player in the home appliance market of Pakistan for almost five decades and is now venturing into real estate sector. This financing will kick start the development of housing project.

The state of the art project is being launched under brand name “Waves Enclave” and will target affordable housing segment of the market with an inventory of more than 1,000 apartments.

This will be located at the entrance of Lahore between Thokar Niaz Baig and Allama Iqbal Town on the main Orange Metro Line.

Top of the line architects and consultants have been hired for the project and it is in the process of required approvals.

Its formal launch is expected in later half this year.

KARACHI: Banks have approved Rs180 billion as loan for low cost housing, the State Bank of Pakistan (SBP) said on Thursday.

The SBP said building upon current momentum, banks have shown strong progress in approving and disbursing the financing under Mera Pakistan Mera Ghar Scheme against the manifold increase in applications by borrowers to avail housing finance.

Up to April 11, 2022, banks received applications for housing finance amounting to Rs409 billion, which was merely Rs57 billion a year ago, reflecting an increase of more than 7 times. Out of these, banks have approved applications amounting to Rs180 billion and disbursed Rs66 billion against the approved applications.

This shows an increase in approvals of applications of more than 11 times as, a year ago, in April 2021, the banks had approved only Rs16 billion.

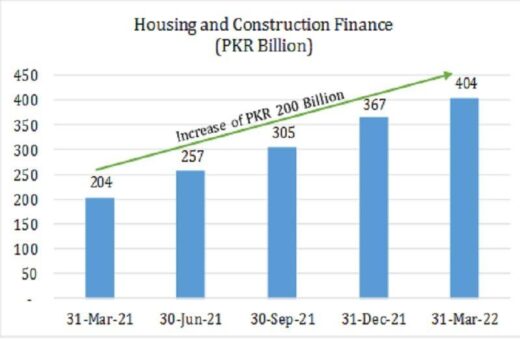

Similar trends can also be observed in the overall financing to the housing and construction sector by banks. Banks almost doubled their housing and construction finance portfolio to Rs404 billion as of March 31, 2022 from Rs204 billion a year earlier. In increasing their housing and construction finance, banks have also achieved, almost 100 per cent, the first quarter target of Rs405 billion for 2022.

To improve provision of financing for the housing and construction sector to increase adequate housing in the country and boost construction sector activities, State Bank of Pakistan (SBP) with the support of Government of Pakistan has taken several measures since July 2020. In October 2020, the Government of Pakistan augmented these efforts by introducing the Government Markup Subsidy Scheme, now commonly known as Mera Pakistan Mera Ghar (MPMG) Scheme. Available in both conventional and Islamic mode, this scheme enables banks to provide financing for the construction and purchase of houses at very low financing rates for low to middle income segments of the population.

Key initiatives taken under MPMG scheme included allowing acceptance of third party guarantee during the construction period, waiver of Debt Burden Ratio (DBR) in case of informal income and the introduction of standard facility offer letter by the banks. SBP also advised banks to develop and deploy income estimation models for borrowers with informal sources of income. In addition to gauge readiness, knowledge and appropriateness of behavior of banking staff towards customers, regular mystery shopping of banking branches were also conducted by State Bank all over the country.

The current progress under MPMG is also attributed to banks’ improved preparedness for handling housing finance that includes alignment of banks’ strategic focus, continued improvements in their systems and procedures, training and capacity building of staff, extensive marketing and leverage of technology to reach out to customers. These improvements have helped banks in better handling of financing requests of potential customers. The huge influx of applications and subsequent approvals of financing by banks under the Scheme indicates that current momentum of disbursements under MPMG will continue in the coming months as well.

STATE BANK OF PAKISTAN

SBP also advised housing and construction finance targets to banks on July 15, 2020. Banks were required to increase their housing and construction finance portfolio to 5 percent of their domestic private sector advances by the end of 2021. As a result, banks’ financing to housing and construction sector increased to Rs367 billion as of December 31, 2021 from Rs148 billion as of June 30, 2020. For 2022, banks have been advised to increase their housing and construction portfolio to 7 percent of their domestic private sector advances i.e. up to Rs560 billion.

The Mera Pakistan Mera Ghar (MPMG) housing scheme received an astounding response during a two-day event in Faisalabad, where banks granted conditional approvals for housing loans totaling approximately Rs7.4 billion.

KARACHI: The State Bank of Pakistan (SBP), in collaboration with banks, is organizing a two-day exhibition in Faisalabad on March 19, 2022 to provide information on house financing.

The State Bank of Pakistan is organizing a two-day Mera Pakistan Mera Ghar (MPMG) Mela at Circle Club Faisalabad on March 19 and 20, 2022, a statement said on Thursday.

In the Mela banks will provide information on the MPMG financing facility whereas builders, developers and real estate agents will showcase the various projects in which the people could purchase housing units or apartments using the financing facility.

The residents of Faisalabad who want to purchase/construct their own house will have an opportunity to obtain information about their eligibility for availing the subsidized housing finance, their monthly installments based on amount of financing and monthly income.

They will also be able to apply for financing from the banks, which may give an in-principal approval then and there provided the required information is provided to them.

The Mela offers free entry and parking for the families besides other attractions including opportunities to win valuable prizes through open draw, daily live music concert by renowned singers, food stalls, and an activity packed fun-area for kids and young ones.

KARACHI: The State Bank of Pakistan (SBP) has revised regulations related to housing loans and general loans mainly related to eligibility of borrowers.

The central bank on Wednesday issued a circular to revise Prudential Regulations for Microfinance Banks.

The SBP said that in order to align classification and provisioning requirements with enhanced loan sizes, it has been decided to revise Prudential Regulations R-5, R-8 and R-10 for MFBs as under;

Regulation R-5: Maximum Loan Size and Eligibility of Borrowers

Maximum loan sizes and borrowers’ income eligibility criteria shall be as under;

General Loans (Other than housing loans): The maximum size for general loans shall be up to Rs. 350,000/- to a poor person with annual income (net of business expenses) up to Rs. 1,200,000/-.

Housing Loans: The maximum size for housing loans shall be up to Rs. 3,000,000/- to a single borrower with annual income (net of business expenses) up to Rs. 1,500,000/-. Further, MFBs shall ensure to implement the following requirements:

(a) General Instructions

i) MFBs shall not allow housing finance purely for the purchase of land/plots; rather, such financing would be extended for the purchase of land/plot and construction on it.

ii) The sanctioned financing limit, assessed on the basis of repayment capacity of the borrower, value of land/plot and cost of construction on it etc. shall be disbursed in tranches.

iii) The amount disbursed for purchase of plot must not exceed the 90 per cent of the market value/cost of land/plot and 50 per cent of the financing limit. The remaining amount shall be disbursed for construction there-upon.

iv) MFBs will take a realistic construction schedule from the borrowers before allowing initial disbursement. For construction-only cases, the sanctioned financing shall also be released in tranches commensurate with the stage of construction.

v) In case of cost overrun, MFBs may entertain the customer for additional finance for completion of house, keeping in view the Debt Burden Ratio (DBR) and cushion in overall Loan-to-Value (LTV) ratio.

(b) Permission from Relevant Authorities

The MFBs shall not disburse housing finance unless ensured that prior permissions/clearances for construction/purchase of property from relevant authorities are available.

(c) Creation of Mortgage

The plot/house/flat financed by the MFBs shall be mortgaged in MFBs’ favour by way of equitable or registered mortgage.

(d) Loan to Value (LTV) Ratio

Loan to Value Ratio should not exceed 90 per cent.

(e) Risk Management and Internal Control Systems

Risk management framework, duly approved by the Board of Directors of MFBs, should appropriately cover housing finance. MFBs shall ensure strict compliance with their internal policies and procedures and those prescribed by SBP from time to time.

(f) Information Disclosure

MFBs shall clearly disclose all the important terms & conditions, fees, charges and penalties etc., which should, inter-alia, include annualized percentage rate, pre-payment penalties and the conditions under which they apply.

For the purpose of this regulation, Annualized Percentage Rate means as follows:

Mark-up for the period

X

365

x

100

Average outstanding principal amount during the period

No. of days

(g) Development of Financing Documentation

The MFBs shall prepare standardized set of financing and recourse documents, duly cleared by their legal counsels, comprising of financing agreement, application form and the other requisite supplementary documents.

(h) Title Documents

MFBs shall obtain all title and ownership related property documents from customers which should be clear and free from all encumbrances/legal charges and get these documents vetted by their legal department/advisor(s). MFBs shall provide a signed copy of the list of all title and property documents to the borrowers.

(i) Verification of Property-related Documents

MFBs shall verify necessary information provided in the application form. Accordingly, all title and other legal documents provided with application form shall be verified directly from the relevant issuing authorities. All the documents shall be kept in safe custody meeting all procedures/requirements.

(j) Property Assessment

MFBs shall ensure that a proper property valuation is done by their internal resources. However, properties valuing above Rs. 3.0 million shall be subject to assessment by valuator on approved panel of Pakistan Banks’ Association.

(k) Insurance/Takaful

MFBs may obtain insurance/takaful coverage of the housing unit financed through a reputable insurance/takaful company to sufficiently cover their risk.

(l) Monitoring of Market Conditions

The management of MFBs shall put in place a mechanism to monitor conditions in housing finance market at least on half-yearly basis to ensure that their policies are aligned with the current market conditions.

Microenterprise Loans:

The maximum size for microenterprise loans shall be up to Rs. 3,000,000/- to a single project or business. The MFBs shall extend the microenterprise loans only in the name of micro entrepreneurs to ensure traceability and reduce the incidence of multiple borrowing. However, the aggregate exposure against the microenterprise loans in excess of ceiling prescribed for general loans shall not exceed 40 per cent of the MFB’s gross loan portfolio.

Pre-requisites for Undertaking Microenterprise Lending:

Only those MFBs that are fully compliant with Minimum Capital Requirement (MCR) and Capital Adequacy Ratio (CAR) shall be eligible to undertake microenterprise lending.

i) MFBs interested to extend microenterprise loans exceeding ceiling prescribed for general loans shall develop related institutional capacity (products, credit risk management and monitoring system, trainings etc.) and submit detailed business plan of microenterprise lending to SBP for seeking necessary approval for pilot program. The SBP shall inter-alia evaluate the plan along with operational/financial performance, funding plan, supervisory assessment, and credit rating of the MFB, and accordingly grant permission for launching pilot program to the applicant MFB.

ii) During the pilot phase MFBs will have to ensure that their aggregate exposure against the microenterprise loans in excess of ceiling prescribed for general loans shall not exceed 20 per cent of the gross loan portfolio. The final approval for undertaking microenterprise lending on full/commercial scale shall be granted subject to satisfactory evaluation of pilot program.

iii) The enhanced loan size (up to Rs. 1,000,000/- and Rs. 3,000,000/- respectively) will be allowed to those MFBs which have graduated from pilot microenterprise lending programs (up to Rs. 500,000/- and Rs. 1,000,000/- respectively) to commercial scale. However, prior to extending microenterprise loans exceeding Rs. 500,000/- and Rs. 1,000,000/-, MFBs shall apply to Agricultural Credit & Microfinance Department, SBP for approval. SBP shall grant approval for pilot/commercial launch based on satisfactory assessment of the capital position and readiness level of the applicant MFB.

Miscellaneous

(a) Income Eligibility Assessment for General & Housing Loans:

While assessing income eligibility on individual borrowers (including salaried persons) for housing & general loans, MFBs shall ensure that the total installment of the financing facilities extended by the financial institutions is commensurate with monthly income and repayment capacity of the borrowers, such that total monthly amortization payments of financing facilities should not exceed 50 per cent of the net disposable income of the prospective borrowers. These measures would be in addition to MFBs’ usual evaluations of each proposal concerning credit worthiness of the borrowers, to ensure that their portfolio fulfills the prudential norms, instructions issued by the State Bank of Pakistan and does not impair the soundness and safety of the MFB itself.

(b) Consumption Financing against the Security of Gold:

In line with SBP’s instructions issued vide AC&MFD Circular No. 02 of 2015 (Annexure I, Para-2), MFBs may also extend loans against gold collateral for consumption purposes categorized as domestic needs/emergency loans. However, MFB’s aggregate loan exposure against the security of gold shall not exceed 35 per cent of its gross loan portfolio.

(c) Asset Liability Mismatches

MFBs shall prudently manage the maturity mismatches arising out of their housing and other long term financing portfolios by raising long-term funds for on-lending and vice versa.

Regulation R-8: Classification of Assets and Provisioning Requirements

A. Specific Provisioning:

The outstanding principal and mark-up of the loans and advances, payments against which are overdue, shall be classified as Non- Performing Loans (NPLs) as prescribed below:

Loan Categories

Time based Criteria for Classification of Assets and Provisioning Requirements

MFBs shall maintain a General Provision equivalent to 1.0 per cent of the net outstanding loans/advances. However, where the loans/advance have been secured against gold and/or other liquid assets, the general provisioning against outstanding amount net of such security shall be required.

C. General Instructions for Classification / Provisioning of all loan categories:

(a) Watch list

MFBs shall maintain a watch list of all overdue accounts before they are classified in terms of objective (time-based) criteria. However, such accounts may not be treated as NPLs for the purpose of classification / provisioning.

(b) Government Guaranteed Loans

Classified loans/ advances that have been guaranteed by the Government would not require provisioning to the extent of guaranteed portion. However, markup/ interest on such accounts would be taken to Memorandum Account instead of Income Account.

(c) Subjective Classification

i) In addition to the time-based criteria prescribed in this regulation, subjective evaluation of performing and non-performing credit portfolio may be made for risk assessment purposes and, where necessary, any account including the performing account can be classified. In this case, the category of classification determined on the basis of time based criteria can be further downgraded.

ii) Classification for program-based lending shall be based on objective (time-based) criteria only, though MFBs, at their own discretion, may also classify such portfolio on subjective basis.

iii) To strengthen subjective classification, MFBs may consider financial standing of guarantors.

(d) Reversal of Specific Provisions

In case of recovery against classified loan, other than rescheduling / restructuring under R-9 of PRs for MFBs, MFBs may reverse/adjust specific provision held against classified assets.

(e) Quarterly Review

MFBs shall review, at least on a quarterly basis, the collectability of their loans / advances portfolio and shall properly document the evaluations so made. Shortfall in provisioning, if any, shall be provided for immediately.

(f) Benefit of Forced Sale Value:

MFBs can avail the benefit of Forced Sale Value (FSV) of collateral held against loans / advances as under:

i) Profit arising from availing the benefit of FSV shall not be available for the payment of cash or stock dividend.

ii) The heads of Credit and Risk of respective MFBs shall ensure that FSV used for taking benefit of provisioning is determined accurately and is reflective of market conditions under forced sale situations.

iii) Borrower-wise details of such cases shall be maintained for verification by SBP. In case of misuse of this facility, SBP may also withdraw the benefit of FSV from the concerned MFB.

(g) Responsibility of the External Auditors

The external auditors shall, as part of their annual audits of MFBs, verify that all requirements, as stipulated in this regulation for classification and provisioning, have been complied with.

The intent of ‘charge-off’ is to clear the balance sheet of MFBs, and this shall in no way extinguish the MFBs’ right of recovery of such loans. NPLs shall be charged off as prescribed below:

Loan Categories

Criteria for Charging Off NPLs

General/Unsecured Loans

NPLs shall be charged off, one month after being classified as “Loss.”

Housing Loans

NPLs shall be charged off, one month after 05 years from the date of classification of financing.

Microenterprise Loans

NPLs secured against Mortgaged residential, commercial and industrial properties (Land & building only) shall be charged off, one month after 05 years from the date of classification. All other NPLs shall be charged off, one month after 03 years from the date of classification.

Note: Charge-off means reducing the value of the loans in ‘loss’ category to zero through offsetting the provisions, thus, removing such loans from the balance sheet.

4. Definitions. To add clarity, following terms have been defined:

(a) Housing Finance means financing provided to individuals for the construction, purchase of residential house/apartment and for purchase of plot and construction thereupon. Financing availed for the purpose of making improvements in house/apartment shall also fall under this category.

(b) Mortgage means transfer of an interest in specific immovable property for the purpose of securing the payment of money advanced or to be advanced by way of loan or finance.

(c) Liquid Assets means assets which are readily convertible into cash without recourse to a court of law and mean encashment/realizable value of government securities, bank deposits, gold ornaments, gold bullion, certificates of deposit, shares of listed companies which are actively traded on the stock exchange, NIT Units, certificates of mutual funds, certificates of investment (COIs) issued by DFIs/NBFCs rated at least ‘A’ by a credit rating agency on the approved panel of SBP, listed TFCs rated at least ‘A’ by a credit rating agency on the approved panel of SBP and certificates of asset management companies for which there is a book maker quoting daily offer and bid rates and there is active secondary market trading. These assets with appropriate margins should be in possession of the MFBs with perfected lien.

(d) Secured means exposure backed by liquid assets, pledged stock, mortgage of land, plant, building, machinery or any other fixed assets, hypothecation of stock (inventory), trust receipt, assignment of receivable, lease rentals, and contract receivables but does not include hypothecation of household goods.

KARACHI: The State Bank of Pakistan (SBP) has relaxed financing conditions for housing units in under construction projects.

The central bank issued a circular dated February 25, 2022 to ease the conditions for house financing. It said that in order to further facilitate buyers of housing units in under construction projects, requirement of builder/developer to avail construction financing is being relaxed.

“Accordingly, purchasers of housing units in under construction projects may avail housing finance against their housing units in projects where builder/developer has not availed construction financing,” the SBP said.

In such cases, the builder/developer will have to create mortgage charge over project’s land in favor of bank/DFI through an agreement. The charge will only be vacated after completion of the project and transfer of housing units to the purchasers. Moreover, the builder/developer will comply with all other provisions of subject guidelines, it added.

Any bank/DFI can provide housing finance to a purchaser of a housing unit in such under construction projects.

However, if the purchaser wants to avail financing from a bank/DFI other than the mortgagee bank/DFI, then it will have to obtain NOC from the mortgagee bank/DFI in this regard.

Moreover, financing bank/DFI of such purchasers will also be required to enter into bilateral arrangement with the mortgagee bank/DFI to secure its risk.

With regard to the requirement of informed consent under guidelines, it is clarified that the builder/developer will be responsible to arrange written informed consent from the customers who intend to purchase housing units from their own sources without availing mortgage finance.

The letters of written consent of such purchasers will be submitted to the bank/DFI in original by the builder/developer.

The builders/developers are developing and marketing a number of multi-storey projects of housing units across the country. Although these under construction projects are exposed to project completion risk and performance risk of builders/developers, many individuals are attracted to book housing units in these projects owing to their affordability and option of payments through installments.

However, the banks/DFIs have traditionally shied away from financing to the housing units in under construction projects due to issues in availability of legally enforceable title documents and registration of mortgages as per requirements of Prudential Regulations (PR) for Housing Finance.

It may be noted that banks/DFIs extend project financing to builders/developers for construction of multistorey housing projects after adequately securing their project and builder risks through mortgage of project land and other securities. Utilizing these already established security arrangements with the builders/developers, the banks/DFIs may also extend housing finance against housing units in multistorey housing projects. This will expand options of affordable housing to the individual borrowers. This will also facilitate banks/DFIs in ensuring repayment/ settlement of their project financing through conversion of the same in housing finance.

A statement said that the central bank had launched dedicated landing webpage on promoting housing and construction finance on its website.

The page contains extensive information on housing and construction finance and Mera Pakistan Mera Ghar (MPMG), Government’s flagship markup subsidy scheme for affordable and low cost housing finance.

The webpage provides information on various measures taken by SBP to promote housing and construction finance such as issuance of separate Prudential Regulations for housing finance, establishment of a high level Steering Committee, allocation of mandatory targets for housing and construction finance, incentives & penalties and market facilitation.

Moreover, a dedicated webpage for MPMG is also available to facilitate the potential applicants who intend to avail housing finance under MPMG.

The MPMG page covers information about the scheme comprehensively including eligibility criteria, tenor of the loan, maximum amount of loan, markup rates to be charged, maximum list of documents required and subsidy being provided by the Government. Through this page, potential applicants can also access websites of participating banks directly wherein loan application forms under various categories are available.

An installment repayment schedule of the loans and an instalment calculator are also available on this webpage.

The webpage also shares monthly data of housing and construction finance extended by the banks. Progress made under MPMG in terms of the latest statistics including data of amount applied, approved and disbursed under MPMG on monthly basis is also available on MPMG webpage.

Visitors will also be able to view the testimonials of the actual borrowers who have availed subsidized housing finance under MPMG by visiting the website. It is expected that this dedicated webpage will facilitate the visitors by providing them actionable information, guidance, and support they require for easy access to financing under MPMG.

ISLAMABAD: Ufone has launched its new state-of-the-art contact center for Pakistan Banks’ Association (PBA). The contact center has been launched to resolve queries and generate leads for the Government of Pakistan’s ‘Mera Pakistan, MeraGhar’ helpline initiative, which brings affordable housing finance facilities for low-income groups.

The Contact Center was inaugurated by Governor, State Bank of Pakistan, Reza Baqir, here in Islamabad, in presence of President and Group CEO, PTCL & Ufone, Hatem Bamatraf, Chairman, Naya Pakistan Housing and Development Authority,Lt. Gen. (Retd.) Anwar Ali Hyder, Chairman Pakistan Banks’ Association (PBA), Muhammad Aurangzeb, and senior management of the member banks and financial institutions of PBA.

Ufone is providing Contact Center services to PBA from two existing Centers by disseminating information on the loan process, eligibility criteria etc., besides offering 24/7 query and complaint resolution services to prospective customers.

Sharing his thoughts at the ceremony, President and Group CEO, PTCL & Ufone, Hatem Bamatraf, said:“We are glad to be a part of this historic initiative for the people of Pakistan. Ufone’s onboarding as the official contact service provider is a testament to the company’s extraordinary track record as a dependable services provider for Pakistan’s business sector. We constantly innovate and modernize our products and services ecosystem to deliver a remarkable user experience to our individual and corporate customers. The latest state-of-the-art Contact Center facility will further enhance our capacity to respond to queries and complaints to bring a hassle-free banking experience to the low-cost housing beneficiaries.”

The Contact Center will provide an additional channel for Ufone to resolve queries and generate leads for the housing finance project and promote its nationwide uptake. The facilities are easily scalable to manage additional facilitation as the need arises.

The facilities feature robust centralized Complaints Management and Leads Management Systems to help the member banks track every step of the customer journey, besides expediting the processing of the loans. Ufone Contact Centers are strategically located for effective management of traffic for calls from across Pakistan.

KARACHI: State Bank of Pakistan (SBP) on Wednesday said that as a result of numerous measures of the SBP and full support of the government, bank lending for the government’s flagship markup subsidy scheme, commonly known as Mera Pakistan Mera Ghar (MPMG), has picked up momentum.

Since the launch of the scheme, applications of Rs 154 billion under MPMG have been received by banks and banks have approved housing finance of over Rs 59 billion up till August 31, 2021. Similarly, the pace of disbursement under MPMG that was initially slow because of a number of factors, including the availability of housing units, has also picked up.

By August 31, 2021, disbursement under the scheme has reached Rs 11.5 billion, showing an increase of around Rs 3.8 billion or 49 per cent in August 2021.

On average, to date banks have approved 38 percent of the amount applied and 19 percent of the approved amount has been disbursed.

These approval and disbursement ratios have similarly risen over the past few months as banks have put in place the needed upfront investment in procedures and technology to process applications for low-cost housing.

It would be pertinent to mention here that banks disbursed amounts in different stages of construction or purchase. Thus the pace of disbursement is contingent upon the speed of construction and completion of the purchasing process.

Since the announcement of MPMG scheme last year, SBP has taken various enabling steps such as introducing standardized and simple application form; adopting an informal income assessment model; providing relaxations in prudential regulations; establishing helpdesks at all SBP field offices; and, designing a complaint portal supported by a network of focal persons of all banks across all geographical areas.

On the instructions of SBP, banks are accepting MPMG applications from over 8,000 dedicated branches across the country. Further, SBP has also allocated targets to each bank under MPMG.

An e-tracking system within each bank and a dedicated joint call center for the facilitation of the applicants have also been established. Naya Pakistan Housing Development Authority (NAPHDA) and Pakistan Banks’ Association (PBA), a representative body of banks, are fully supporting MPMG.

It is expected that with the ongoing efforts by SBP, Government, and Banks, bank finance for MPMG will gain further momentum in the days to come.

KARACHI: State Bank of Pakistan (SBP) on Thursday issued guidelines for financing the housing units in under-construction projects.

The SBP said that builders/developers are developing and marketing a number of multistorey projects of housing units across the country.

Although these under-construction projects are exposed to project completion risk and performance risk of builders/developers, many individuals are attracted to book housing units in these projects owing to their affordability and option of payments through installments.

However, the banks/DFIs have traditionally shied away from financing the housing units in under-construction projects due to issues in the availability of legally enforceable title documents and registration of mortgages as per requirements of Prudential Regulations (PR) for Housing Finance.

It may be noted that banks/DFIs extend project financing to builders/developers for the construction of multistorey housing projects after adequately securing their project and builder risks through mortgage of project land and other securities.

Utilizing these already established security arrangements with the builders/developers, the banks/DFIs may also extend housing finance against housing units in multistorey housing projects.

This will expand options of affordable housing to individual borrowers. This will also facilitate banks/DFIs in ensuring repayment/ settlement of their project financing through conversion of the same in housing finance.

In view of the above considerations, State Bank has decided to issue guidelines to encourage banks/DFIs to extend housing finance to the housing units in under-construction projects for which they have already entered into arrangements of project financing with builders/developers.

These Guidelines for Financing of Housing Units in Under-construction Projects have been developed considering current market norms of buying/selling of housing units in under-construction projects by addressing issues of legally enforceable rights and responsibilities.

While guidelines comprehensively cover various aspects, it may be noted that all payments to the builder/developer for completion of construction/project shall be routed through an escrow account maintained by the bank/lead bank of the consortium.

The builder’s/developer’s equity and purchasers’ equity contribution and subsequent payments of the purchasers through mortgage financing shall be routed through the same account.

Accordingly, the State Bank has decided to exempt banks/DFIs extending housing finance for under-construction housing units from requirements as specified under Regulation HF 8: Creation of Mortgage for Housing Finance.

This exemption will be available till the arrangement of the completion certificate, NOCs, approvals, utility connections, and registered title deed between builder/developer and buyers of housing units. In order to avail of this exemption, the banks/DFIs will, however, be required to meticulously comply with provisions of Guidelines for Financing of Housing Units in Under-construction Projects.