In a move aimed at enhancing revenue generation during the current fiscal year, Pakistan has implemented new amendments to both direct and indirect tax laws.

(more…)Tag: Income Tax Ordinance 2001

-

Pakistan enhances income tax rates for banks

ISLAMABAD: Pakistan has enhanced tax rates for banks through amendments introduced through Finance Act, 2022.

In this regard the apex tax agency of the country, i.e. Federal Board of Revenue (FBR) on Thursday issued Income Tax Circular No. 15 of 2022/2023 to explain important amendments made to Income Tax Ordinance, 2001 through Finance Act, 2022.

READ MORE: Declaring beneficial owner made mandatory for companies, AOPs

The FBR said that tax rates for banking companies are enhanced as explained hereunder:

The taxable income arising from additional income of banking companies earned from additional investment in Federal Government securities for tax year 2020 and 2021 was taxable at the rate of 37.5 per cent instead of rates provided in Division II of Part I of First Schedule of the Income Tax Ordinance, 2001.

READ MORE: Pakistan reintroduces capital value tax on motor vehicles

This provision was further amended through Finance Act, 2021, whereby income attributable to investment in the Federal Government securities of banking companies was made taxable on the basis of advances to deposit ratios at graduated tax rates of 40 per cent, 37.5 per cent and 35 per cent, if ratio was up to 40 per cent, 40-50 per cent and above 50 per cent respectively.

The Finance Act, 2022 has introduced enhanced rates of tax on taxable income of banks attributable to investment in Federal Government securities.

READ MORE: Customs duty exemption, concession granted

The enhanced rates for tax year 2022 are 55 per cent, 49 per cent and 35 per cent if gross advances to deposit ratio was upto 40 per cent, 40-50 per cent or above 50 per cent respectively.

For tax year 2023, and onwards tax rates will be 55 per cent, 49 per cent and 39 per cent if gross advances to deposit ratio is up to 40 per cent, 40 -50 per cent or above 50 per cent respectively.

The changes have been incorporated by substituting sub-rule (6A) of rule 6C of Seventh Schedule to the Ordinance.

READ MORE: Commodities’ illegal movement to be treated as smuggling

The tax rate on income of banking companies has been enhanced to 39 per cent for tax year 2023 from current 35 per cent through amendment in Division II of Part I of First Schedule of the Ordinance.

Additionally, the application of section 4B has been restricted up to tax year 2022 in case of banking companies.

-

Key changes to income tax laws through Finance Act 2022

KARACHI: The Finance Act, 2022 has made significant changes to Income Tax Ordinance, 2001, which are applicable from July 01, 2022.

Following are the significant changes in Income Tax Ordinance, 2001 through Finance Act, 2022 as explained by PwC A.F. Ferguson & Co.:

READ MORE: Non-ATL retailers to pay double amount of fixed tax

1. Slab rates for super tax introduced for taxpayers having income in excess of Rs 150 million. The Bill earlier proposed such threshold at Rs 300 million at a standard rate of 2 per cent.

2. Super tax rate is enhanced to 10 per cent for certain specified sectors for tax year 2022 whereas for banking companies such enhanced rate of super tax will be applicable for tax year 2023.

READ MORE: Tampering PSW data to attract 4-year jail sentence

3. The proposal of final tax regime for commercial importers is withdrawn. Consequently, commercial importers will remain under minimum tax regime.

4. The proposal to restrict income tax holiday of certain IPPs withdrawn.

5. The standard rate of tax for banking companies revised at 39 per cent.

READ MORE: NA approves levy on petroleum products up to Rs50/liter

6. The revised slab rates for salaried individuals introduced by setting below taxable limit at Rs 600,000 as against the original proposal of Rs 1,200,000. Further, the reduction in tax rates proposed in Finance Bill has not only been reversed but the tax incidence has also been enhanced (as compared to position prior to Finance Bill).

7. The right to carry forward minimum tax retained, however, the period is reduced from five to three years.

8. The tax credit on contributions to Voluntary Pension Scheme retained.

9. The resident individual will now also include a citizen of Pakistan who was not in any one foreign country for more than 182 days.

10. The credit for income covered by final tax in respect of assets declared in wealth statement or books of account in excess of imputable income is inter alia subject to submission of audited financial statements.

READ MORE: All tax proposals of IT sector accepted: FBR

11. Advance tax on sale of immovable properties to be collected irrespective of holding period.

12. The rate of advance tax on imports mentioned in Part II of the Twelfth Schedule enhanced from 2 per cent to 3.5 per cent.

13. Reduced rate of Capital Gains Tax on listed securities based on holding period to apply on securities purchased on or after July 01, 2022.

-

Advance tax on immovable property purchase enhanced to 250% for non-filers

ISLAMABAD: Pakistan has announced a sharp increase in advance tax on purchase of immovable property to 250 per cent for persons not filing income tax returns.

The country presented budget 2022/2023 on June 10, 2022 and announced various taxation measures to boost revenue collection.

The Finance Bill, 2022 proposed the sharp increase in advance tax for persons not filing tax returns. The decision has been taken to further burden the persons not complying with the statutory requirements.

READ MORE: Pakistan massively increases taxation on motor vehicles

The bill proposed amendment in Section 236K of Income Tax Ordinance, 2001. According to the proposed amendment:

“Provided further that the tax required to be collected under section 236K shall be increased by two hundred and fifty percent of the rate specified in Division XVIII of Part IV of the First Schedule in case of persons not appearing in the active taxpayers.”

At present the buyer, in case of filer of income tax return, of immovable property is required to pay advance tax at 1 per cent of the value. However, in case of non-filer the rate shall be enhanced by 100 per cent or 2 per cent as envisaged under Tenth Schedule of the Income Tax Ordinance, 2001.

READ MORE: New rates of capital gain tax on disposal of securities

According to the Ordinance updated up to June 30, 2021, following is the text of Section 236K:

236K. Advance tax on purchase or transfer of immovable property.—(1) Any person responsible for registering, recording or attesting transfer of any immovable property shall at the time of registering, recording or attesting the transfer shall collect from the purchaser or transferee advance tax at the rate specified in Division XVIII of Part IV of the First Schedule.

Explanation,—For removal of doubt, it is clarified that the person responsible for registering, recording or attesting transfer includes person responsible for registering, recording or attesting transfer for local authority, housing authority, housing society, co-operative society, public and private real estate projects registered/governed under any law, joint ventures, private commercial concerns and registrar of properties.

(2) The advance tax collected under sub-section (1) shall be adjustable:

READ MORE: Pakistan slaps 45% corporate tax on banks

Provided that if the buyer or transferee is a non-resident individual holding a Pakistan Origin Card (POC) or National ID Card for Overseas Pakistanis (NICOP) or Computerized National ID Card (CNIC) who has acquired the said immovable property through a Foreign Currency Value Account (FCVA) or NRP Rupee Value Account (NRVA) maintained with authorized banks in Pakistan under the foreign exchange regulations issued by the State Bank of Pakistan, the tax collected under this section from such persons shall be final discharge of tax liability for such buyer or transferee.

(3) Any person responsible for collecting payments in installments for purchase or allotment of any immovable property where the transfer is to be effected after making payment of all installments, shall at the time of collecting installments collect from the allotee or transferee advance tax at the rate specified in Division XVIII of Part IV of the First Schedule:

READ MORE: Tax rates for business individuals, AOPs during TY2023

Provided that where tax has been collected along with installments, no further tax under this section shall be collected at the time of transfer of property in the name of buyer from whom tax has been collected in installments which is equal to the amount payable in this section.

(4) Nothing contained in this section shall apply to a scheme introduced by the Federal Government, or Provincial Government or an Authority established under a Federal or Provincial law for expatriate Pakistanis:

“Provided that the mode of payment by the expatriate Pakistanis in the said scheme or schemes shall be in the foreign exchange remitted from outside Pakistan through normal banking channels.”

READ MORE: Pakistan reintroduces advance tax on foreign payments

-

Pakistan massively increases taxation on motor vehicles

ISLAMABAD: Pakistan has massively increased the amount of tax on purchase of motor vehicles from July 01, 2022.

The country presented its federal budget 2022/2023 on June 10, 2022 and took various taxation measures to boost revenue collection.

Finance Minister Miftah Ismail while presenting the budget stated that in continuation of our policy to shift the burden of tax on the rich class, advance tax on motor vehicles exceeding 1600cc is proposed to be increased.

READ MORE: New rates of capital gain tax on disposal of securities

Furthermore, advance tax shall also be collected at the rate of 2 per cent of the value in cases of high value hybrid and electric vehicles. Additionally, the rate of tax for non-filers shall be enhanced to 200 per cent from the current 100 per cent.

Accordingly, the Finance Bill, 2022 proposed the following new rates of advance tax on registration of motor vehicles from July 01, 2022:

S.No Engine Capacity Tax (1) (2) (3) 1. Upto 850 cc Rs.10,000 2. 851cc to 1000cc Rs.20,000 3. 1001cc to 1300cc Rs.25,000 4. 1301cc to 1600cc Rs.50,000 5. 1601cc to 1800cc Rs.150,000 6. 1801cc to 2000cc Rs.200,000 7. 2001cc to 2500cc Rs.300,000 8. 2501cc to 3000cc Rs.400,000 9. Above 3000cc Rs.500,000 According to the Finance Bill, 2022, provided that in cases where engine capacity is not applicable and the value of vehicle is Rupees five million or more, the rate of tax collectible shall be 3% of the import value as increased by customs duty, sales tax and federal excise duty in case of imported vehicles or invoice value in case of locally manufactured or assembled vehicles.”

READ MORE: Pakistan slaps 45% corporate tax on banks

It further said: “Provided that the tax required to be collected under section 231B shall be increased by two hundred percent of the rate specified in First Schedule in case of persons not appearing in the active taxpayers’ list.”

READ MORE: Advance tax on private motor vehicles

The existing rates of advance tax on motor vehicles are (for filers and it will increase by 100 per cent in case of non-filer of income tax returns):

1. upto 850cc: Rs. 7,500

2. 851cc to 1000cc: Rs. 15,000

3. 1001cc to 1300cc: Rs. 25,000

4. 1301cc to 1600cc: Rs. 50,000

5. 1601cc to 1800cc: Rs. 75,000

6. 1801cc to 2000cc: Rs. 100,000

7. 2001cc to 2500cc: Rs. 150,000

8. 2501cc to 3000cc: Rs. 200,000

9. Above 3000cc: Rs. 250,000]

-

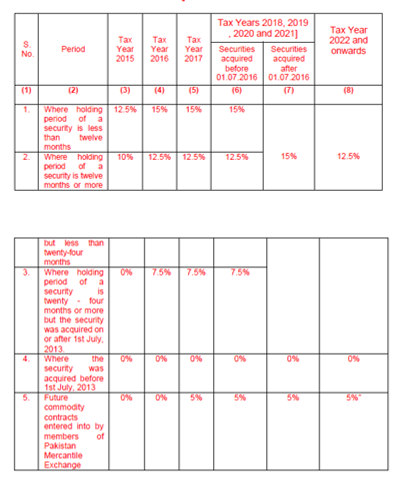

New rates of capital gain tax on disposal of securities

ISLAMABAD: The government has proposed new rates of capital gain tax on disposal of securities traded at Pakistan Stock Exchange (PSX).

Pakistan presented its federal budget on June 10, 2022 and introduced various taxation measures to boost revenue collection.

READ MORE: Pakistan slaps 45% corporate tax on banks

Through Finance Bill, 2022 proposed to revise the rates of capital gain tax for tax year 2023 and onwards.

Following is the proposed rates of capital gain tax:

S.No Holding Period Rate of Tax for Tax year 2023 and onwards (1) (2) (3) 1. Where the holding period does not exceed one year 15% 2. Where the holding period exceeds one year but does not exceed two years 12.5% 3. Where the holding period exceeds two years but does not exceed three years 10% 4. Where the holding period exceeds three years but does not exceed four years 7.5% 5. Where the holding period exceeds four years but does not exceed five years 5% 6. Where the holding period exceeds five years but does not exceed six years 2.5% 7. Where the holding period exceeds six years 0% 8. Future commodity contracts entered into by members of Pakistan Mercantile Exchange 5%”; The Federal Board of Revenue (FBR) collects capital gain tax on disposal of securities under Section 37A of the Income Tax Ordinance, 2001.

Following is the text of Section 37A of Income Tax Ordinance, 2001:

READ MORE: Tax rates for business individuals, AOPs during TY2023

37A. Capital gain on disposal of securities.—(1) The capital gain arising on or after the first day of July 2010, from disposal of securities, other than a gain that is exempt from tax under this Ordinance, shall be chargeable to tax at the rates specified in Division VII of Part I of the First Schedule:

Provided that this section shall not apply to a banking company and an insurance company.

(1A) The gain arising on the disposal of a security by a person shall be computed in accordance with the following formula, namely: —

A – B

Where —

(i) ‘A’ is the consideration received by the person on disposal of the security; and

READ MORE: Pakistan reintroduces advance tax on foreign payments

(ii) ‘B’ is the cost of acquisition of the security.

(2) The holding period of a security, for the purposes of this section, shall be reckoned from the date of acquisition (whether before, on or after the thirtieth day of June, 2010) to the date of disposal of such security falling after the thirtieth day of June, 2010.

(3) For the purposes of this section “security” means share of a public company, voucher of Pakistan Telecommunication Corporation, Modaraba Certificate, an instrument of redeemable capital,debt Securities, unit of exchange traded fund and derivative products.

(3A) For the purpose of this section, “debt securities” means –

READ MORE: Exchange companies to withhold tax on payment to MTOs

(a) Corporate Debt Securities such as Term Finance Certificates (TFCs), Sukuk Certificates (Sharia Compliant Bonds), Registered Bonds, Commercial Papers, Participation Term Certificates (PTCs) and all kinds of debt instruments issued by any Pakistani or foreign company or corporation registered in Pakistan; and

(b) Government Debt Securities such as Treasury Bills (T-bills), Federal Investment Bonds (FIBs), Pakistan Investment Bonds (PIBs), Foreign Currency Bonds, Government Papers, Municipal Bonds, Infrastructure Bonds and all kinds of debt instruments issued by Federal Government, Provincial Governments, Local Authorities and other statutory bodies.

“Explanation: For removal of doubt it is clarified that derivative products include future commodity contracts entered into by the members of Pakistan Mercantile Exchange whether or not settled by physical delivery.”

(3B) For the purpose of this section, “shares of a public company” shall be considered as security if such company is a public company at the time of disposal of such shares.

(4) Gain under this section shall be treated as a separate block of income.

(5) Notwithstanding anything contained in this Ordinance, where a person sustains a loss on disposal of securities in a tax year, the loss shall be set off only against the gain of the person from any other securities chargeable to tax under this section and no loss shall be carried forward to the subsequent tax year:

Provided that so much of the loss sustained on disposal of securities in tax year 20l9 and onwards that has not been set off against the gain of the person from disposal of securities chargeable to tax under this section shall be carried forward to the following tax year and set off only against the gain of the person from disposal of securities chargeable to tax under this section, but no such loss shall be carried forward to more than three tax years immediately succeeding the tax year for which the loss was first computed.

(6) To carry out purpose of this section, the Board may prescribe rules.

The rate of tax to be paid under section 37A shall be as follows:—

-

Pakistan slaps 45% corporate tax on banks

ISLAMABAD: Pakistan has slapped corporate income tax at 45 per cent on banks, which is raised from 35 per cent.

The country presented its federal budget on June 10, 2022 and introduced tax measures for boosting revenue collection.

READ MORE: Tax rates for business individuals, AOPs during TY2023

Through Finance Bill, 2022 the tax rate for banking companies have been proposed to increase to 45 per cent from existing 35 per cent.

In this regard, the bill proposed amendment to Division II, Part I of First Schedule of the Income Tax Ordinance, 2001.

Proposed Rates of Tax for Companies

READ MORE: Pakistan reintroduces advance tax on foreign payments

The rate of tax imposed on the taxable income of a company shall be as set out in the following Table, namely:-

Type of Company Rate of Tax Small company 20% Banking company 45% Any other company 29% Following are the existing rates of tax for corporate entities for tax year 2022:

(i) The rate of tax imposed on the taxable income of a company for the tax year 2007 and onward shall be 35%:

Provided that the rate of tax imposed on the taxable income of a company other than a banking company, shall be 34% for the tax year 20145:

READ MORE: Exchange companies to withhold tax on payment to MTOs

Provided further that the rate of tax imposed on the taxable income of a company, other than a banking company, shall be 33% for the tax year 2015:

“Provided further that the rate of tax imposed on taxable income of a company, other than banking company shall be 32% for the tax year 2016, 31% for tax year 2017, 30% for tax year 2018 and 29% for tax year 2019 and onwards.

READ MORE: Salaried persons denied adjustments against deduction

(iii) where the taxpayer is a small company as defined in section 2, tax shall be payable at the rate of 25%:

Provided that for tax year 2019 and onwards tax rates shall be as set out in the following Table, namely:—

Tax year Rate of Tax 2019 24% 2020 23% 2021 22% 2022 21% 2023 and onwards 20%” -

Tax rates for business individuals, AOPs during TY2023

ISLAMABAD: Finance Bill, 2022 has proposed to revise tax rates for business individuals and Association of Persons (AOPs) during Tax year 2023.

The government presented its federal budget 2022/2023 and introduced various changes to taxation laws to ensure documentation and plug revenue leakages.

READ MORE: Pakistan reintroduces advance tax on foreign payments

Through Finance Bill, 2022 the basic exemption of tax on income of individuals and AOPs has been increased to Rs600,000 from Rs400,000.

Following is the proposed tax card for business individuals and AOPs.

READ MORE: Exchange companies to withhold tax on payment to MTOs

Sr. No. Taxable Income Rate of Tax 1. Where taxable income does not exceed Rs. 600,000/ 0 per cent 2. Where taxable income exceeds Rs. 600,000 but does not exceed Rs. 800,000 5 per cent of the amount exceeding Rs. 600,000 3. Where taxable income exceeds Rs. 800,000 but does not exceed Rs. 1,200,000 Rs. 10,000 + 12.5 per cent of the amount exceeding Rs. 800,000 4. Where taxable income exceeds Rs. 1,200,000 but does not exceed Rs. 2,400,000 Rs.60,000 + 17.5 per cent of the amount exceeding Rs. 1,200,000 5. Where taxable income exceeds Rs. 2,400,000 but does not exceed Rs. 3,000,000 Rs. 270,000 + 22.5 per cent of the amount exceeding Rs. 2,400,000 6. Where taxable income exceeds Rs. 3,000,000 but does not exceed Rs. 4,000,000 Rs. 405,000 + 27.5 per cent of the amount exceeding Rs. 3,000,000 7. Where taxable income exceeds Rs. 4,000,000 but does not exceed Rs. 6,000,000 Rs. 680,000 + 32.5 per cent of the amount exceeding Rs. 4,000,000 8. Where taxable income exceeds Rs. 6,000,000 Rs. 1,330,000 + 35 per cent of the amount exceeding Rs. 6,000,000.” Following are the existing rates of tax for Individuals and Association of Persons for tax year 2022:

READ MORE: Salaried persons denied adjustments against deduction

(1) Subject to clause (2), the rates of tax imposed on the income of every individual and association of persons except a salaried individual shall be as set out in the following Table, namely:—

1. Where taxable income does not exceed Rs. 400,000: the tax rate shall be zero per cent.

2. Where the taxable income exceeds Rs. 400,000 but does not exceed Rs. 600,000: the tax rate shall be 5 per cent of the amount exceeding Rs. 400,000.

3. Where taxable income exceeds Rs. 600,000 but does not exceed Rs. 1,200,000: the tax rate shall be Rs. 10,000 plus 10 per cent of the amount exceeding Rs. 600,000.

4. Where taxable income exceeds Rs.1,200,000 but does not exceed Rs. 2,400,000: the tax rate shall be Rs. 70,000 plus 15 per cent of the amount exceeding Rs. 1,200,000.

READ MORE: New ADR mechanism introduced to facilitate taxpayers

5. Where taxable income exceeds Rs. 2,400,000 but does not exceed Rs. 3,000,000: the tax rate shall be Rs. 250,000 plus 20 per cent of the amount exceeding Rs. 2,400,000.

6. Where taxable income exceeds Rs. 3,000,000 but does not exceed Rs. 4,000,000: the tax rate shall be Rs. 370,000 plus 25 per cent of the amount exceeding Rs. 3,000,000.

7. Where taxable income exceeds Rs. 4,000,000 but does not exceed Rs. 6,000,000: the tax rate shall be Rs. 620,000 plus 30 per cent of the amount exceeding Rs. 4,000,000.

8. Where taxable income exceeds Rs. 6,000,000: the tax rate shall be Rs. 1,220,000 plus 35 per cent of the amount exceeding Rs. 6,000,000.

-

Pakistan reintroduces advance tax on foreign payments

ISLAMABAD: Pakistan has reintroduced advance tax on foreign payments made through credit, debit or prepaid cards. The advance tax has been revived through Finance Bill, 2022.

The country presented its federal budget 2022/2023 on June 10, 2022 and made several amendments in tax laws to broaden tax base and plug revenue leakages.

READ MORE: Exchange companies to withhold tax on payment to MTOs

The Finance Bill, 2022 proposed to reintroduce Section 236Y of the Income Tax Ordinance, 2001. The section was omitted through Finance Act, 2021.

Following is the proposed amendment in the Income Tax Ordinance, 2001:

READ MORE: Salaried persons denied adjustments against deduction

“236Y. Advance tax on persons remitting amounts abroad through credit or debit or prepaid cards.—(1) Every banking company shall collect advance tax, at the time of transfer of any sum remitted outside Pakistan, on behalf of any person who has completed a credit card or debit card or prepaid card transaction with a person outside Pakistan at the rate specified in Division XXVII of Part IV of the First Schedule.

READ MORE: New ADR mechanism introduced to facilitate taxpayers

(2) The advance tax collected under this section shall be adjustable.”

The Finance Bill 2022 proposed advance tax rate on amount remitted abroad through credit, debit or prepaid cards under section 236Y shall be 1 per cent of the gross amount remitted abroad.

READ MORE: FBR to disable mobile SIMs on non-filing of tax returns

-

Exchange companies to withhold tax on payment to MTOs

ISLAMABAD: Exchange companies have been brought under the ambit of withholding tax and now they are required to deduct tax on payment to international money transfer operators (MTOs).

The change has been proposed through budget 2022/2023, which was presented on June 10, 2022.

Through Finance Bill, 2022 amendments suggested to Section 152 of the Income Tax Ordinance, 2001.

READ MORE: Salaried persons denied adjustments against deduction

According to amendments, new sub-sections have been proposed:

“(1DC) Every exchange company licensed by the State Bank of Pakistan shall deduct tax at the time of making payment of service charges or commission or fee, by whatever name called, to the global money transfer operators, international money transfer operators or such other persons engaged in international money transfers or cross-border remittances for facilitating outward remittances, at the rates given in Division IV, Part I of the First Schedule:

READ MORE: New ADR mechanism introduced to facilitate taxpayers

Provided that where such person retains service charges or commission or fee, by whatever name called from the amount payable to the exchange company on any account, the exchange company shall be deemed to have paid the service charges or commission or fee, by whatever name called and the exchange company shall collect the tax accordingly.

(1DD) Every banking company while making payment to card network company or payment gateway or any other person, of any transaction fee or licensing fee or service charges or commission or fee by whatever name called or interbank financial telecommunication services, shall deduct tax at the rates given in Division IV, Part I of the First Schedule:

READ MORE: FBR to disable mobile SIMs on non-filing of tax returns

Provided that where card network company or payment gateway or any other person retains money in relation to aforementioned services from the amount payable to the banking company on any account, the banking company shall be deemed to have paid the amount and the banking company shall collect the tax accordingly.”;

According to Income Tax Ordinance, 2001 updated up to June 30, 2021, the rate of tax imposed under section 6 on payments to non-residents shall be 15 per cent of the gross amount of the royalty or fee for technical services and 5 per cent of the gross amount of the fee for offshore digital services.

READ MORE: Pakistan amends tax laws to legalize money transfers