The Federal Board of Revenue is Pakistan’s apex tax agency, overseeing tax collection and policies. Pakistan Revenue is committed to providing timely updates on the Federal Board of Revenue to its readers.

ISLAMABAD: Federal Board of Revenue (FBR) has issued updated rates of duty and tax for customs clearance of imported vehicle.

The Federal Government of Pakistan has extended various benefits / exemptions to the taxpayers for importing vehicles, according to updated rates up to June 30, 2020.

The details concessions / exemptions are given as under:-

i. S.R.O. 577(I)/2005 Dated 06.06.2005 (Exemption from customs duty, sales tax, withholding tax on import of certain specified Old and used automotive vehicles)

The import of old and used automotive vehicles of Asian makes meant for transport of persons, specified in column (2) of the Table below, falling under PCT heading No. 87.03 of the First Schedule to the Customs Act, 1969 (IV of 1969), is exempted from so much of the customs-duty, sales tax and withholding tax as are in excess of the cumulative amount specified in column (3) thereof,

Sr. No

Automotive vehicles of Asian makes meant for transport of persons.

Duty and taxes in US$ or equivalent amount in Pak rupees.

(1)

(2)

(3)

1

Up to 800cc

US$4800

2

Up to 801-1000cc

US$6000

3

From 1001 – 1300cc

US$13200

4

From 1301 – 1500cc

US$18590

5

From 1501 – 1600cc

US$22550

6

From 1601 – 1800cc (Excluding Jeeps)

US$27940

It is relevant to mention that the Federal Government has fixed the leviable duty and taxes of automotive vehicles of Asian makes meant for transport of persons as discussed above irrespective of their physical condition. The Customs officers do not have any discretionary power to increase / decrease the leviable duties / taxes, the FBR said.

Watch this story on Youtube. Please subscribe the channel:

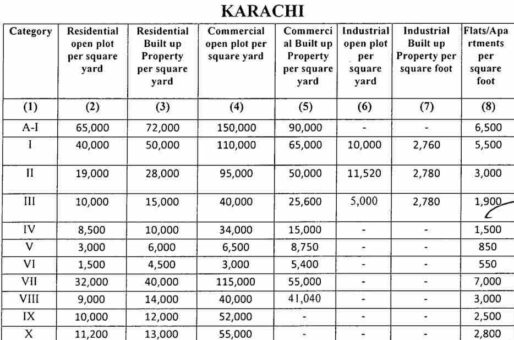

ISLAMABAD: Following is the table of valuation of immovable properties in Karachi issued by the Federal Board of Revenue (FBR) for the purpose of deduction and collection of withholding tax.

The valuation of immovable properties in Karachi has been issued through SRO 837(I)/2019 dated July 23, 2019 in supersession of notification SRO 120(I)/2019 dated February 01, 2019.

The valuation of immovable properties is applicable from July 24, 2019.

The FBR said that:

(i) Values in the above table are in rupees;

(ii) value is per square yard of the covered area of ground floor plus covered area for the additional floors;

(iii) commercial property built up value is per square yard of the covered area of the ground floor plus covered area of the additional floors, if any;

(iv) built up industrial property value is per square yard of the plot area per square foot;

(v) the value in respect of a residential building consisting of more than one storey shall be increased by 25 percent for each additional storey i.e. value of each storey other than ground floor shall be calculated at 25 percent of the value of the ground floor;

(vi) a property which does not appear to fall in any of the categories shown in the Appendix below shall be deemed to fall in the adjacent lowest category of the Appendix;

(vii) whether the land has been granted for more than one purpose. Viz residential, commercial and industrial, the valuation in such a case shall be the mean/average prescribed rate;

(viii) a flat means the covered residential tenement having separate property unit number / sub-property unit number;

(ix) in residential, multi storey building, additional storey shall be charged if it consists of bed room and bath room;

(x) the rates for basements of built in commercial property in categories I, II, III and IV shall be Rs13,500 per square yard; and

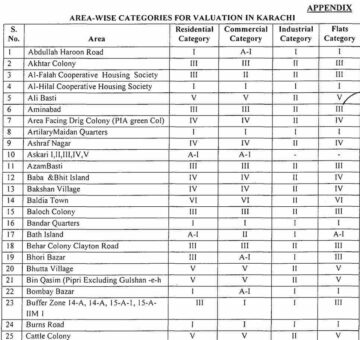

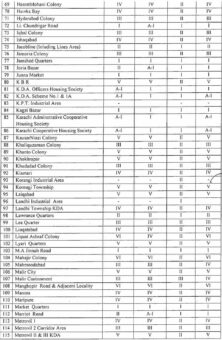

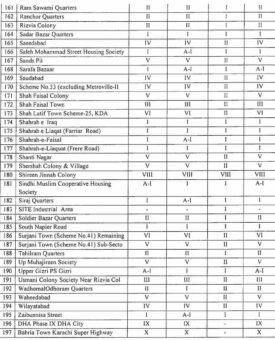

(xi) area-wise categories are in the following appendix

ISLAMABAD: Federal Board of Revenue (FBR) on Friday constituted a provincial complaint resolution committee for settlement of issues relating of sales tax refund matters for Khyber Pakhtunkhwa (KPK).

The FBR constituted the complaint resolution committee Khyber Pakhtunkhwa comprising following members for settlement of sales tax refund issues for taxpayers falling under the jurisdiction of field formations of Khyber Pakhtunkhwa:

ISLAMABAD – A tax amnesty providing relief on undeclared money to builders and developers for new housing projects is set to expire on December 31, 2020.

ISLAMABAD: Federal Board of Revenue (FBR) has issued updated list of Tier-1 retailers, who have integrated their Point of Sales (POS) with the online system of the tax authorities.

Only a customer of Tier-1 retailer is eligible to get cash back of five percent sales tax out of total amount of sales tax paid at the time of purchase from such retailers.

All tier-1 retailers are required to integrate all their POSs with FBR’s computerized system. ‘Tier-1 retailer’ is defined in section 2(43A) of the Sales Tax Act, 1990, to be a person who falls in any of the following categories:

(a) a retailer operating as a unit of a national or international chain of stores;

(b) a retailer operating in an air-conditioned shopping mall, plaza or centre, excluding kiosks;

(c) a retailer whose cumulative electricity bill during the immediately preceding twelve consecutive months exceeds Rupees twelve hundred thousand;

(d) a wholesaler-cum-retailer, engaged in bulk import and supply of consumer goods on wholesale basis to the retailers as well as on retail basis to the general body of the consumers”; and

(e) a retailer, whose shop measures one thousand square feet in area or more.

Following is the list of Tier-1 retailers who integrated their POS with the FBR:

001. RANA TRADING COMPANY (RTC)

002. HI GOLD INTERNATIONAL ENTERPRISES

003. IFFI ELECTRONICS

004. M/S:- TAYYAB SUPER STORE & BUILDERS

005. AFZAL ELECTRONICS

006. AL HAFEEZ ELECTRONICS

007. M/S SEASONS FOODS PRIVATE LIMITED

008. MUNAWAR ASSOCIATES

009. TEAM-A VENTURE (PRIVATE) LIMITED

010. TAFRAL NIAZI TRADERS

011. MS ZUBAIDA ASSOCIATES

012. M/S SUPER ASIA ELECTRONICS,

013. M/S 3-STAR TRADING COMPANY,

014. REWAYAT

015. SEATS

016. TAZ & CO.

017. BIZTECH INTERNATIONAL

018. RETAIL 21

019. WOW SOLUTION (PVT.) LIMITED

020. PAKISTAN ELECTRONICS.

021. AL FALAH SWEETS & BAKERS

022. HAQ’S INTERNATIONAL

023. HOUSE OF CHARIZMA

024. RETAIL CONCEPTS.

025. TILE SELECT (PRIVATE) LIMITED

026. SAVE’N SAVE (PVT) LIMITED

027. SULAFAH

028. WORLD EELCTRONICS

029. KAHF INTERNATIONAL.

030. SAVE MART I-8

031. SAUDA SULF.

032. SHAHEEN CHEMIST

033. KHADIJA ENTERPRISES

034. SPEED (PRIVATE) LIMITED

035. M/S UNITED RETAIL (SMC-PRIVATE) LIMITED

036. H KARIM BUKSH ENTERPRISES

037. M/S PENSY GARMENTS (PVT) LTD

038. M/S PUNJAB CASH AND CARRY BAHRIA TOWN PHASE 4

ISLAMABAD: Federal Board of Revenue (FBR) on Wednesday issued procedure for cash back five percent sales tax to customers, which is paid at the time of payment to Tier-1 retailers.

The FBR issued SRO 1339(I)/2020 dated December 16, 2020 to make amendment in Sales Tax Rules, 2006.

Following is the procedure for payment of five percent sales tax paid on purchases made by customers of Tier-1 retailers:

(1) All customers of Tier-1 retailers are entitled to redeem 5 percent of the sales tax paid as cash back on eligible goods of the tax amount as inscribed on the invoice issued by the Teir-1 retailers.

(2) To redeem under sub-rule (1) the cash online, the customer shall log on to the mobile application.

(3) Soon after log on under sub-rule (2), an independent FBR wallet account shall be created for each customer.

(4) Approved outlet shall also create an independence FBR wallet account for each customer.

(5) An identical FBR wallet account shall be created for each point of sale by the approved outlet.

(6) The customer shall verify the electronically generated invoice through the mobile application.

(7) As soon as the electronically generated invoice is verified, the system shall automatically calculate the 5 percent amount of the tax paid on the invoice.

(8) The customer shall transfer the amount determined under sub-rule (7) into his FBR wallet account.

(9) The customer may redeem the earned amount within one month of his purchases accumulated in his FBR wallet account on any approved outlet who shall refund the amount accumulated in the wallet account of the customer after ensuring that the earned amount is transferred from the customer’s wallet account to the approved outlets wallet account.

(10) The approved outlet shall adjust the amount so refunded to the customer which shall be automatically uploaded from the approved outlet’s wallet account to the sales tax return of the approved outlet for the relevant tax period by auto adjusting the output tax liability.

ISLAMABAD: Federal Board of Revenue (FBR) has launched an online module to facilitate investor to apply online for grant of Greenfield industry status, a FBR spokesman said on Wednesday.

To promote investment in the Greenfield Industry and to facilitate such investors, Federal Board of Revenue (FBR) has launched online module in Iris for facilitating filing of applications for the grant of Greenfield Industry Status.

To this end, two separate applications have been provided under the Income Tax Ordinance, 2001 and Sales Tax Act, 1990.

Faceless compliance and facilitation through the use of ICT tools is a priority agenda of FBR as per the Vision of the Present government.

FBR is moving fast to accomplish this vision as a leader in developing and launching such faceless compliance tools for facilitation of the taxpayers.

ISLAMABAD: Federal Board of Revenue (FBR) on Wednesday issued draft amendment for notifying format for updating profile by taxpayers.

The FBR issued SRO 1341(I)/2020 dated December 16, 2020 to issue draft amendment to Income Tax Rules, 2002.

A new rule 34B has been proposed for taxpayer’s profile. The FBR said that this rule shall apply for the purpose of section 114A of the Income Tax Ordinance, 2001, which provides for the furnishing of a taxpayer’s profile.

A taxpayer’s profile shall be filed electronically on the prescribed format and manner as provided on IRIS web portal.

The taxpayer’s profile shall be verified in the manner specified on IRIS web portal.

Through Finance Act, 2020 a new section 114A was inserted to Income Tax Ordinance, 2001 for making it mandatory for taxpayers to update their profile.

Following is the text of Section 114A:

Section 114A: Taxpayer’s profile.

(1) Subject to this Ordinance, the following persons shall furnish a profile, namely:-

(a) every person applying for registration under section 181;

(b) every person deriving income chargeable to tax under the head, “Income from business”;

(c) every person whose income is subject to final taxation;

(d) any non-profit organization as defined in clause (36) of section 2;

(e) any trust or welfare institution; or

(f) any other person prescribed by the Board.

(2) A taxpayer’s profile-

(a) shall be in the prescribed form and shall be accompanied by such annexures, statements or documents as may be prescribed;

(b) shall fully state, in the specified form and manner, the relevant particulars of –

(i) bank accounts;

(ii) utility connections;

(iii) business premises including all manufacturing, storage or retail outlets operated or leased by the taxpayer;

(iv) types of businesses; and

(v) such other information as may be prescribed;

(c) shall be signed by the person being an individual, or the person’s representative where section 172 applies; and

(d) shall be filed electronically on the web prescribed by the Board.

(3) A taxpayer’s profile shall be furnished,-

(a) on or before the 31st day of December, 2020 in case of a person registered under section 181 before the 30th day of September, 2020; and

(b) within ninety days registration in case of a person not registered under section 181 before the 30th day of September, 2020.

(4) A taxpayer’s profile shall be updated within ninety days of change in any of the relevant particulars of information as mentioned in clause (b) of sub-section (2).

ISLAMABAD: Federal Board of Revenue (FBR) on Wednesday issued procedure for conducting electronic audit by officers of Inland Revenue.

An amendment was introduced to Sales Tax Act, 1990 through Finance Act, 2020 under which commissioner of Inland Revenue authorized to conduct audit proceedings electronically through video link or any other facility as prescribed by the FBR.

The FBR now made amendments to Sales Tax Rules, 2006 to implement the law introduced through Finance Act, 2020.

The FBR said where a case has been selected under section 25 or section 72B of the Sales Tax Act, 1990, as the case may be, and the competent authority issues directions to conduct e-audit, the following procedure shall be adopted:

(a) the concerned commissioner Inland Revenue shall serve a notice under sub-section (1) of Section 25 of the Act to the registered person specifying the reasons for selection of his case for audit;

(b) The commissioner Inland Revenue having jurisdiction shall assign the case to an audit officer to conduct e-audit.

(c) A registered person shall produce the record as required to be maintained under section 22 of the act through IRIS or an electronic data carrier as notified by the Board;

(d) a registered person shall not be required to appear either personally or through authorized representative in connection with any proceedings under e-audit before the audit officer:

Provided that a registered person may request for an opportunity of personal hearing through IRIS and such hearings shall be conducted exclusively through video links from personal computer system or any of the nearest tax facilitation center situated at the premises of the field formations.

(e) the audit officer after considering all the information, documents or evidence, if the audit officer finds no discrepancy and have no conclusive proof against registered person, he may close the audit in IRIS under intimation to the commission inland revenue having jurisdiction;

(f) after completion of audit, examination of record and obtaining registered person’s explanation on all the issues raised, if the audit officer does not agree with the declared version, he shall prepare an audit report, containing audit observations and finding. The audit officer shall forward the report to the commissioner Inland Revenue having jurisdiction and also send a copy of it to the registered person through IRIS;

(g) the commissioner inland revenue having jurisdiction shall assign the case to an adjudication officer to make an order for assessment of tax under section 11, including imposition of penalty and default surcharge in accordance with section 33 and 34 of the Act;

(h) on the basis of the audit report referred to in sub-rule (e), the adjudicating officer shall issue a show cause notice through IRIS to the registered person; and

(i) the adjudicating officer may, if considered necessary, after obtaining the registered person’s explanation on all the issues raised in the audit report, pass an order under section 11 of the act.