ISLAMABAD: Federal Board of Revenue (FBR) has updated rates of tax on capital gain on disposal of immovable properties that are applicable during tax year 2021 (July 01, 2020 – June 30, 2021).

The FBR issued Income Tax Ordinance, 2001 (updated June 30, 2020) after incorporating amendments brought through Finance Act, 2020. The FBR updated the following rate of tax on Capital Gains on disposal of Immovable Property.

The rate of tax to be paid under sub-section (1A) of section 37 shall be as follows:—

S.No.

Amount of Gain

Rate of tax

(1)

(2)

(3)

1.

Where the gain does not exceed Rs. 5 million

2.5%

2.

Where the gain exceeds Rs. 5 million but does not exceed Rs. 10 million

5%

3.

Where the gain exceeds Rs. 10 million but does not exceed Rs. 15 million

ISLAMABAD: Federal Board of Revenue (FBR) has updated rates of tax on income from property to be applicable during tax year 2021 (July 01, 2020 to June 30, 2021).

The FBR issued Income Tax Ordinance, 2001 (updated till June 30, 2020) incorporating amendments brought through Finance Act, 2020. Through the ordinance, the FBR updated the rate of tax to be paid under section 15, in the case of individual and association of persons, shall be as follows:-

S.No.

Gross amount of rent

Rate of tax

(1)

(2)

(3)

1.

Where the gross amount of rent does not exceed Rs.200,000.

Nil

2.

Where the gross amount of rent exceeds Rs.200,000 but does not exceed Rs.600,000.

5 per cent of the gross amount exceeding Rs.200,000.

3.

Where the gross amount of rent exceeds Rs.600,000 but does not exceed Rs.1,000,000.

Rs.20,000 plus 10 per cent of the gross amount exceeding Rs.600,000.

4.

Where the gross amount of rent exceeds Rs.1,000,000 but does not exceed Rs. 2,000,000.

Rs.60,000 plus 15 per cent of the gross amount exceeding Rs1,000,000.

5.

Where the gross amount of rent exceeds Rs.2,000,000 but does not exceed Rs. 4,000,000.

Rs.210,000 plus 20 per cent of the gross amount exceeding Rs.2,000,000

6.

Where the gross amount of rent exceeds Rs. 4,000,000 but does not exceed Rs. 6,000,000

Rs.610,000 plus 25 per cent of the gross amount exceeding Rs.4,000,000

7.

Where the gross amount of rent exceeds Rs. 6000,000 but does not exceeds Rs. 8,000,000

Rs.1,110,000 plus 30 per cent of the gross amount exceeding Rs.6,000,000

8.

Where the gross amount of rent exceeds Rs. 8,000,000

Rs.1,710,000 plus 35 percent of the gross amount exceeding Rs.8,000,000

KARACHI: Federal Board of Revenue (FBR) has updated tax rate for profit on debt to be applicable during tax year 2021 (July 01, 2020 – June 30, 2021).

The FBR issued Income Tax Ordinance, 2001 (updated June 30, 2020) after incorporating amendments brought through Finance Act, 2020. The FBR updated following rate of tax on profit on debt.

The rate of tax for profit on debt imposed under section 7B shall be—

S.NO

Profit on Debt

Rate of tax

(1)

(2)

(3)

1.

Where profit on debt does not exceed Rs.5,000,000

15%

2.

Where profit on debt exceeds Rs.5,000,000 but does not exceed Rs.25,000,000

17.5%

3.

Where profit on debt exceeds Rs.25,000,000 but does not exceed Rs. 36,000,000

20%

The tax rate is deducted under Section 7B of Income Tax Ordinance, 2001, under which:

Section 7B. Tax on profit on debt.—(1) Subject to this Ordinance, a tax shall be imposed, at the rate specified in Division IIIA of Part I of the First Schedule, on every person, other than a company, who receives a profit on debt from any person mentioned in clauses (a) to (d) of sub-section (1)of section 151.

(2) The tax imposed under sub-section (1) on a person, other than a company, who receives a profit on debt shall be computed by applying the relevant rate of tax to the gross amount of the profit on debt.

(3) This section shall not apply to a profit on debt that –

ISLAMABAD: Federal Board of Revenue (FBR) has updated income tax rate on dividend received from a company during tax year 2021 (July 01, 2020 – June 30, 2021).

The FBR issued Income Tax Ordinance, 2001 (updated up to June 30, 2020) incorporating amendments brought through Finance Act, 2020. The FBR updated following rate of dividend tax:

The rate of tax imposed under section 5 on dividend received from a company shall be-

(a) 7.5 percent in the case of dividends paid by Independent Power Producers where such dividend is a pass through item under an Implementation Agreement or Power Purchase Agreement or Energy Purchase Agreement and is required to be re-imbursed by Central Power Purchasing (CPPA-G) or its predecessor or successor entity.

(b) 15 percent in mutual funds and cases other than those mentioned in clauses (a) and (c).

(c) 25 percent in case of a person receiving dividend from a company where no tax payable by such company, due to exemption of income or carry forward of business losses under Part VIII of Chapter III or claim of tax credits under Part X of Chapter III.

Section 5 of Income Tax Ordinance, 2001 explains tax on dividends as:

Section 5. Tax on dividends.— (1) Subject to this Ordinance, a tax shall be imposed, at the rate specified in Division III of Part I of the First Schedule, on every person who receives a dividend from a company or treated as dividend under clause (19) of section 2.

(2) The tax imposed under sub-section (1) on a person who receives a dividend shall be computed by applying the relevant rate of tax to the gross amount of the dividend.

(3) This section shall not apply to a dividend that is exempt from tax under this Ordinance.

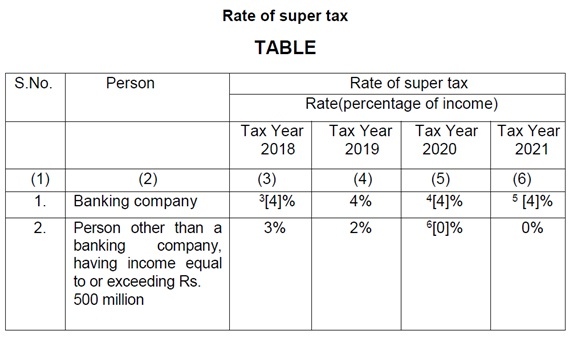

ISLAMABAD: Federal Board of Revenue (FBR) has updated rate of super tax to be applicable for tax year 2021 (July 01, 2020 – June 30, 2021).

The FBR issued Income Tax Ordinance, 2001 after incorporating amendment brought through Finance Act, 2020. The FBR issued the following updated rate of super tax:

Provided that in case of a banking company, super tax for tax year 2019 shall be payable, on estimate basis, by thirtieth day of June, 2018.

Super tax was introduced through Finance Act, 2015 by inserting Section 4B to Income Tax Ordinance, 2001.

The section 4B is read as:

4B. Super tax for rehabilitation of temporarily displaced persons.― (1) A super tax shall be imposed for rehabilitation of temporarily displaced persons, for tax years 2015 and onwards, at the rates specified in Division IIA of Part I of the First Schedule, on income of every person specified in the said Division.

(2) For the purposes of this section, “income” shall be the sum of the following:—

(i) profit on debt, dividend, capital gains, brokerage and commission;

(ii) taxable income (other than brought forward depreciation and brought forward business losses) under section (9) of this Ordinance, if not included in clause (i);

(iii) imputable income as defined in clause (28A) of section 2 excluding amounts specified in clause (i); and

(iv) income computed, other than brought forward depreciation, brought forward amortization and brought forward business lossess under Fourth, Fifth, Seventh and Eighth Schedules.

(3) The super tax payable under sub-section (1) shall be paid, collected and deposited on the date and in the manner as specified in sub-section (1) of section 137 and all provisions of Chapter X of the Ordinance shall apply.

(4) Where the super tax is not paid by a person liable to pay it, the Commissioner shall by an order in writing, determine the super tax payable, and shall serve upon the person, a notice of demand specifying the super tax payable and within the time specified under section 137 of the Ordinance.

(5) Where the super tax is not paid by a person liable to pay it, the Commissioner shall recover the super tax payable under subsection (1) and the provisions of Part IV,X, XI and XII of Chapter X and Part I of Chapter XI of the Ordinance shall, so far as may be, apply to the collection of super tax as these apply to the collection of tax under the Ordinance.

(6) The Board may, by notification in the official Gazette, make rules for carrying out the purposes of this section.

ISLAMABAD: Federal Board of Revenue (FBR) has issued rates of income tax for companies to be applicable during tax year 2021.

The FBR issued Income Tax Ordinance, 2001 (updated June 30, 2020) incorporating amendments brought through Finance Act, 2020.

The FBR said that the rate of tax shall be 29 percent on the taxable income of a company for tax year 2021.

As per the Income Tax Ordinance, 2001, the tax rate on corporate entities has been defined as:

The rate of tax imposed on the taxable income of a company for the tax year 2007 and onward shall be 35 percent:

Provided that the rate of tax imposed on the taxable income of a company other than a banking company, shall be 34 percent for the tax year 2014:

Provided further that the rate of tax imposed on the taxable income of a company, other than a banking company, shall be 33 percent for the tax year 2015:

Provided further that the rate of tax imposed on taxable income of a company, other than banking company shall be 32 percent for the tax year 2016, 31 percent for tax year 2017, 30 percent for tax year 2018 and 29 percent for tax year 2019 and onwards.

Where the taxpayer is a small company as defined in section 2 of Income Tax Ordinance, 2001, tax shall be payable at the rate of 25 percent:

Provided that for tax year 2019 and onwards tax rates shall be as set out in the following Table, namely:—

ISLAMABAD: Federal Board of Revenue (FBR) has issued tax rates to be applicable on business individuals and Association of Persons (AOPs) during tax year 2021.

The FBR issued Income Tax Ordinance, 2001 (updated June 30, 2020) incorporating amendment brought through Finance Act, 2020.

The FBR said that the rates of tax imposed on income of every individual and association of persons except a salaried individual shall be as set out in the following Table, namely:—

S. No.

Taxable income

Rate of tax

(1)

(2)

(3)

1.

Where taxable income does not exceed Rs. 400,000

0%

2.

Where the taxable income exceeds Rs. 400,000 but does not exceed Rs. 600,000

5% of the amount exceeding Rs. 400,000

3.

Where taxable income exceeds Rs. 600,000 but does not exceed Rs. 1,200,000

Rs. 10,000 plus 10% of the amount exceeding Rs. 600,000

4.

Where taxable income exceeds Rs.1,200,000 but does not exceed Rs. 2,400,000

Rs. 70,000 plus 15% of the amount exceeding Rs. 1,200,000

5.

Where taxable income exceeds Rs. 2,400,000 but does not exceed Rs. 3,000,000

Rs. 250,000 plus 20% of the amount exceeding Rs. 2,400,000

6.

Where taxable income exceeds Rs. 3,000,000 but does not exceed Rs. 4,000,000

Rs. 370,000 plus 25% of the amount exceeding Rs. 3,000,000

7.

Where taxable income exceeds Rs. 4,000,000 but does not exceed Rs. 6,000,000

Rs. 620,000 plus 30% of the amount exceeding Rs. 4,000,000

8.

Where taxable income exceeds Rs. 6,000,000

Rs. 1,220,000 plus 35% of the amount exceeding Rs. 6,000,000

The Federal Board of Revenue (FBR) has updated the income tax rates for salaried individuals for the tax year 2021. These rates, which have been incorporated into the Income Tax Ordinance, 2001, as amended by the Finance Act, 2020, will remain applicable from July 1, 2020, to June 30, 2021, unless further amendments are made.

ISLAMABAD: Federal Board of Revenue (FBR) has updated advance tax rates for registration and transfer of motor vehicles during tax year 2021.

The FBR issued the tax rates as updated up to June 30, 2020 and will remain applicable during July 01, 2020 to June 30, 2021, if not amended.

The advance tax on motor vehicles at the time of registration and transfer of registration is governed under Section 231B of Income Tax Ordinance, 2001, which states:

Section 231B. Advance tax on private motor vehicles.—

(1) Every motor vehicle registering authority of Excise and Taxation Department shall collect advance tax at the time of registration of a motor vehicle, at the rates specified in Division VII of Part IV of the First Schedule:

“Provided that no collection of advance tax under this sub-section shall be made after five years from the date of first registration as specified in clauses (a), (b) and (c) of sub-section (6).”

(1A) Every leasing company or a scheduled bank or a non-banking financial institution or an investment bank or a modaraba or a development finance institution, whether shariah compliant or under conventional mode, at the time of leasing of a motor vehicle to a “person whose name is not appearing in the active taxpayers’ list”, either through ijara or otherwise, shall collect advance tax at the rate of four per cent of the value of the motor vehicle.

(2) Every motor vehicle registering authority of Excise and Taxation Department shall collect advance tax at the time of transfer of registration or ownership of a private motor vehicle, at the rates specified in Division VII of Part IV of the First Schedule:

Provided that no collection of advance tax under this sub-section shall be made on transfer of vehicle after five year from the date of first registration in Pakistan.

(3) Every manufacturer of a motor “vehicle” shall collect, at the time of sale of a motor car or jeep, advance tax at the rate specified in Division VII of Part IV of the First Schedule from the person to whom such sale is made.

(4) Sub-section (1) shall not apply if a person produces evidence that tax under sub-section (3) in case of a locally manufactured vehicle or tax under section 148 in the case of imported vehicle was collected from the same person in respect of the same vehicle.

(5) The advance tax collected under this section shall be adjustable:

Provided that the provisions of this section shall not be applicable in the case of –

(a) the Federal Government;

(b) a Provincial Government;

(c) a Local Government;

(d) a foreign diplomat; or

(e) a diplomatic mission in Pakistan.

“(6) For the purposes of this section the expression “date of first registration” means—

(a) the date of issuance of broad arrow number in case a vehicle is acquired from the Armed Forces of Pakistan;

(b) the date of registration by the Ministry of Foreign Affairs in case the vehicle is acquired from a foreign diplomat or a diplomatic mission in Pakistan;

(c) the last day of the year of manufacture in case of acquisition of an unregistered vehicle from the Federal or a Provincial Government; and

(d) in all other cases the date of first registration by the Excise and Taxation Department.

(7) For the purpose of this section “motor vehicle” includes car, jeep, van, sports utility vehicle, pick-up trucks for private use, caravan automobile, limousine, wagon and any other automobile used for private purpose.”

Explanation.— For the removal of doubt, it is clarified that a motor vehicle does not include a rickshaw, motorcycle-rickshaw and any other motor vehicle having engine capacity upto 200cc.

(1) The rate of tax under sub-sections (1) and (3) of section 231B shall be as set out in the following Table:–

S. No.

Engine capacity

Tax

(1)

(2)

(3)

1.

upto 850cc

Rs. 7,500

2.

851cc to 1000cc

Rs. 15,000

3.

1001cc to 1300cc

Rs. 25,000

4.

1301cc to 1600cc

Rs. 50,000

5.

1601cc to 1800cc

Rs. 75,000

6.

1801cc to 2000cc

Rs. 100,000

7.

2001cc to 2500cc

Rs. 150,000

8.

2501cc to 3000cc

Rs. 200,000

9.

Above 3000cc

Rs. 250,000

(2) The rate of tax under sub-sections (2) of section 231B shall be as follows:–

S. No.

Engine capacity

Tax

(1)

(2)

(3)

1.

upto 850cc

–

2.

851cc to 1000cc

5,000

3.

1001cc to 1300cc

7,500

4.

1301cc to 1600cc

12,500

5.

1601cc to 1800cc

18,750

6.

1801cc to 2000cc

25,000

7.

2001cc to 2500cc

37,500

8.

2501cc to 3000cc

50,000

9.

Above 3000cc

62,500

Provided that the rate of tax to be collected shall be reduced by 10 percent each year from the date of first registration in Pakistan.