ISLAMABAD: Federal Board of Revenue (FBR) has updated rate of super tax to be applicable for tax year 2021 (July 01, 2020 – June 30, 2021).

The FBR issued Income Tax Ordinance, 2001 after incorporating amendment brought through Finance Act, 2020. The FBR issued the following updated rate of super tax:

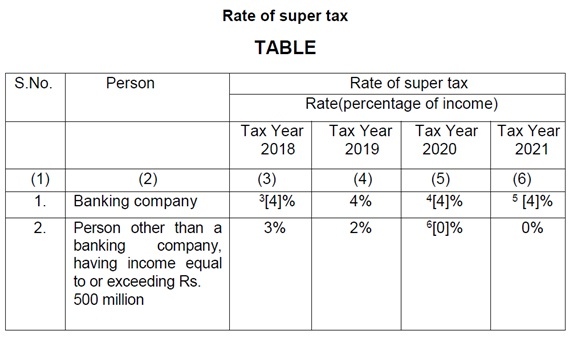

Provided that in case of a banking company, super tax for tax year 2019 shall be payable, on estimate basis, by thirtieth day of June, 2018.

Super tax was introduced through Finance Act, 2015 by inserting Section 4B to Income Tax Ordinance, 2001.

The section 4B is read as:

4B. Super tax for rehabilitation of temporarily displaced persons.― (1) A super tax shall be imposed for rehabilitation of temporarily displaced persons, for tax years 2015 and onwards, at the rates specified in Division IIA of Part I of the First Schedule, on income of every person specified in the said Division.

(2) For the purposes of this section, “income” shall be the sum of the following:—

(i) profit on debt, dividend, capital gains, brokerage and commission;

(ii) taxable income (other than brought forward depreciation and brought forward business losses) under section (9) of this Ordinance, if not included in clause (i);

(iii) imputable income as defined in clause (28A) of section 2 excluding amounts specified in clause (i); and

(iv) income computed, other than brought forward depreciation, brought forward amortization and brought forward business lossess under Fourth, Fifth, Seventh and Eighth Schedules.

(3) The super tax payable under sub-section (1) shall be paid, collected and deposited on the date and in the manner as specified in sub-section (1) of section 137 and all provisions of Chapter X of the Ordinance shall apply.

(4) Where the super tax is not paid by a person liable to pay it, the Commissioner shall by an order in writing, determine the super tax payable, and shall serve upon the person, a notice of demand specifying the super tax payable and within the time specified under section 137 of the Ordinance.

(5) Where the super tax is not paid by a person liable to pay it, the Commissioner shall recover the super tax payable under subsection (1) and the provisions of Part IV,X, XI and XII of Chapter X and Part I of Chapter XI of the Ordinance shall, so far as may be, apply to the collection of super tax as these apply to the collection of tax under the Ordinance.

(6) The Board may, by notification in the official Gazette, make rules for carrying out the purposes of this section.