The tax rates on disposal of securities for tax year 2022 under the First Schedule of the Income Tax Ordinance, 2001.

The Federal Board of Revenue (FBR) issued the Income Tax Ordinance, 2001 updated up to June 30, 2021. The Ordinance incorporated amendments brought through Finance Act, 2021.

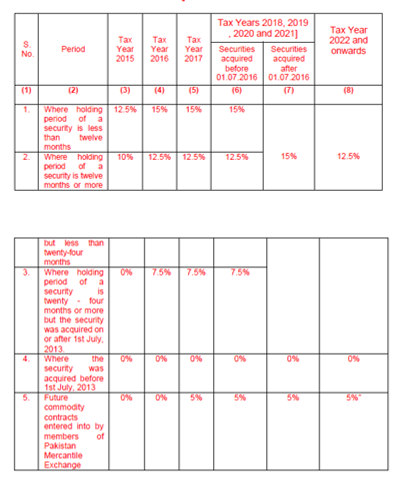

Following are the rates on disposal of securities:

The rate of tax to be paid under section 37A shall be as follows:—

TABLE I

Provided that the rate of tax on cash settled derivatives traded on the stock exchange shall be 5% for the tax years 2018 to 2020.

Provided that the rate for companies shall be as specified in Division II of Part I of First Schedule, in respective of debt securities;

Provided further that a mutual fund or a collective investment scheme or a REIT scheme shall deduct Capital Gains Tax at the rates as specified below, on redemption of securities as prescribed, namely:—

| Category | Rate |

| Individual and association of persons | 10% for stock funds 10% for other funds |

| Company | 10% for stock funds 25% for other funds |

Explanation.- For removal of doubt, it is clarified that, the provisions of this proviso shall be applicable only in case of a mutual fund or collective investment scheme or a REIT scheme.