The Federal Board of Revenue is Pakistan’s apex tax agency, overseeing tax collection and policies. Pakistan Revenue is committed to providing timely updates on the Federal Board of Revenue to its readers.

ISLAMABAD: Federal Board of Revenue (FBR) has granted concession of Rs24.14 billion as sale tax on domestic supply of sugar.

According to official documents, the FBR granted concession of Rs24.41 billion on supply of domestic sales of sugar to end consumers during tax year 2020.

The concession was granted as reduced rate of eight percent on sales of the commodity made by sugar mills under 8th schedule of Sales Tax Act, 1990.

The FBR said that the beneficiary of this concessional rate was general public.

Under the reduce rate of sales tax under 8th Schedule, the FBR granted tax relief of Rs35.45 billion on consumer items mainly food items.

The details of the tax relief revealed that an amount of Rs6.77 billion was granted as sales tax concession to soya bean meal as industrial input.

Further an amount of Rs2.58 billion has been granted as tax concession on ingredients of poultry feed, cattle feed, except soya bean meal of PCT heading 2304.0000 and oilcake of cotton-seed falling under PCT heading 2306.1000.

ISLAMABAD: Federal Board of Revenue (FBR) has signed agreement with Punjab province to get land ownership data for broadening the tax base.

In line with the vision of the Prime Minister to improve transparency in the tax collection system, FBR has achieved another milestone by signing an MoU with the Board of Revenue, Punjab.

Under the MoU, Board of Revenue, Punjab will share the data with Federal Board of Revenue which includes E-Stamps on a number of transactions and land ownership data.

FBR has been making consistent efforts to acquire third party data by linking its IT Systems with such parties to broaden tax base and to improve the transparency in the collection system.

ISLAMABAD: Federal Board of Revenue (FBR) has updated rates of minimum tax to be applicable during tax year 2021 (July 01, 2020 – June 30, 2021).

The FBR issued Income Tax Ordinance, 2001 (updated up to June 30, 2020) after incorporating amendment brought through Finance Act, 2020. The FBR updated following rates of minimum tax under Section 113 of the Ordinance:

S.No

Person(s)

Minimum Tax as percentage of the person’s turnover for the year

(1)

(2)

(3)

1.

(a) Oil marketing companies, Oil refineries, Sui Southern Gas Company Limited and Sui Northern Gas Pipelines Limited (for the cases where annual turnover exceeds rupees one billion.) (b) Pakistani Airlines; and (c) Poultry industry including poultry breeding, broiler production, egg production and poultry feed production. (d) Dealers or distributors of fertilizer ; and (e) person running an online marketplace as defined in clause (38B) of section 2.

0.75%

2.

(a) Distributors of pharmaceutical products, fast moving consumer goods and cigarettes; (b) Petroleum agents and distributors who are registered under the Sales Tax Act, 1990; (c) Rice mills and dealers; and (d) Flour mills.

0.25%

3.

Motorcycle dealers registered under the Sales Tax Act, 1990.

0.3%

4.

In all other cases.

1.5%

Section 113: Minimum tax on the income of certain persons.

(1) This section shall apply to a resident company, permanent establishment of a non-resident company, an individual (having turnover of ten million rupees or above in the tax year 2017 or in any subsequent tax year) and an association of persons (having turnover of ten million rupees or above in the tax year 2017 or in any subsequent tax year) where, for any reason whatsoever allowed under this Ordinance, including any other law for the time being in force—

(a) loss for the year;

(b) the setting off of a loss of an earlier year;

(c) exemption from tax;

(d) the application of credits or rebates; or

(e) the claiming of allowances or deductions (including depreciation and amortization deductions) no tax is payable or paid by the person for a tax year or the tax payable or paid by the person for a tax year is less than the percentage as specified in column (3) of the Table in Division IX of Part-I of the First Schedule of the amount representing the person’s turnover from all sources for that year:

Explanation.-For the purpose of this sub-section, the expression “tax payable or paid” does not include-

(a) tax already paid or payable in respect of deemed income which is assessed as final discharge of the tax liability under section 169 or under any other provision of this Ordinance; and

(b) tax payable or paid under section 4B.”

(3) Where this section applies:

(a) the aggregate of the person’s turnover as defined in sub-section (3) for the tax year shall be treated as the income of the person for the year chargeable to tax;

(b) the person shall pay as income tax for the tax year (instead of the actual tax payable under this Ordinance), minimum tax computed on the basis of rates as specified in Division IX of Part I of First Schedule;

(c) where tax paid under sub-section (1) exceeds the actual tax payable under Part I, clause (1) of Division I, or Division II of the First Schedule, the excess amount of tax paid shall be carried forward for adjustment against tax liability under the aforesaid Part of the subsequent tax year:

Provided that the amount under this clause shall be carried forward and adjusted against tax liability for five tax years immediately succeeding the tax year for which the amount was paid.

(4) “turnover” means,-

(a) the gross sales or gross receipts, exclusive of Sales Tax and Federal Excise duty or any trade discounts shown on invoices,

or bills, derived from the sale of goods, and also excluding any amount taken as deemed income and is assessed as final discharge of the tax liability for which tax is already paid or payable;

(b) the gross fees for the rendering of services for giving benefits including commissions; except covered by final discharge of tax liability for which tax is separately paid or payable;

(c) the gross receipts from the execution of contracts; except covered by final discharge of tax liability for which tax is separately paid or payable; and

(d) the company’s share of the amounts stated above of any association of persons of which the company is a member.

ISLAMABAD: Federal Board of Revenue (FBR) has updated rates of tax on capital gain on disposal of immovable properties that are applicable during tax year 2021 (July 01, 2020 – June 30, 2021).

The FBR issued Income Tax Ordinance, 2001 (updated June 30, 2020) after incorporating amendments brought through Finance Act, 2020. The FBR updated the following rate of tax on Capital Gains on disposal of Immovable Property.

The rate of tax to be paid under sub-section (1A) of section 37 shall be as follows:—

S.No.

Amount of Gain

Rate of tax

(1)

(2)

(3)

1.

Where the gain does not exceed Rs. 5 million

2.5%

2.

Where the gain exceeds Rs. 5 million but does not exceed Rs. 10 million

5%

3.

Where the gain exceeds Rs. 10 million but does not exceed Rs. 15 million

ISLAMABAD: Federal Board of Revenue (FBR) has updated rates of tax on income from property to be applicable during tax year 2021 (July 01, 2020 to June 30, 2021).

The FBR issued Income Tax Ordinance, 2001 (updated till June 30, 2020) incorporating amendments brought through Finance Act, 2020. Through the ordinance, the FBR updated the rate of tax to be paid under section 15, in the case of individual and association of persons, shall be as follows:-

S.No.

Gross amount of rent

Rate of tax

(1)

(2)

(3)

1.

Where the gross amount of rent does not exceed Rs.200,000.

Nil

2.

Where the gross amount of rent exceeds Rs.200,000 but does not exceed Rs.600,000.

5 per cent of the gross amount exceeding Rs.200,000.

3.

Where the gross amount of rent exceeds Rs.600,000 but does not exceed Rs.1,000,000.

Rs.20,000 plus 10 per cent of the gross amount exceeding Rs.600,000.

4.

Where the gross amount of rent exceeds Rs.1,000,000 but does not exceed Rs. 2,000,000.

Rs.60,000 plus 15 per cent of the gross amount exceeding Rs1,000,000.

5.

Where the gross amount of rent exceeds Rs.2,000,000 but does not exceed Rs. 4,000,000.

Rs.210,000 plus 20 per cent of the gross amount exceeding Rs.2,000,000

6.

Where the gross amount of rent exceeds Rs. 4,000,000 but does not exceed Rs. 6,000,000

Rs.610,000 plus 25 per cent of the gross amount exceeding Rs.4,000,000

7.

Where the gross amount of rent exceeds Rs. 6000,000 but does not exceeds Rs. 8,000,000

Rs.1,110,000 plus 30 per cent of the gross amount exceeding Rs.6,000,000

8.

Where the gross amount of rent exceeds Rs. 8,000,000

Rs.1,710,000 plus 35 percent of the gross amount exceeding Rs.8,000,000

KARACHI: Dr. Muhammad Ashfaq, Member Inland Revneue (Operations), Federal Board of Revenue (FBR) on Saturday said video surveillance is solution for monitoring of production without human intervention.

He was addressing the members of Karachi Chamber of Commerce and Industry (KCCI). He said that although the chamber had criticized the implementation of video surveillance. But there is no other solution for monitoring, he added.

He said that industries had shown intention for video analytics. He said that the sugar industry had serious production issues. He further said that the world had adopted technology. The FBR is also adopting advanced technology and the industry should accept it, he added.

The Member said that FBR was the only implementing agency and the laws were made in the Parliament.

Dr. Ashfaq said that the FBR had released refunds to the tune of Rs250 billion during the past six months.

He said that the country needs better public finance. Therefore, the FBR was focusing on increasing the tax net. The broadening of the tax base would also reduce burden on the existing taxpayers, he added.

On the occasion, Siraj Kassem Teli, Chairman, Businessmen Group (BMG) said that an amount of around Rs1830 billion was stuck up in litigation. He suggested that these cases should be resolved on priority basis.

He said that many cases were framed against taxpayers only to meet tax collection targets.

He offered business community support in broadening the tax base.

KCCI President Shariq Vohra said that the FBR should focus on revenue collection instead harassing the taxpayers.

He said that the FBR was taking help from SROs to generate additional revenue. The notifications and SROs are creating difficulties for the business community as well as for tax machinery.

KARACHI: Federal Board of Revenue (FBR) has updated tax rate for profit on debt to be applicable during tax year 2021 (July 01, 2020 – June 30, 2021).

The FBR issued Income Tax Ordinance, 2001 (updated June 30, 2020) after incorporating amendments brought through Finance Act, 2020. The FBR updated following rate of tax on profit on debt.

The rate of tax for profit on debt imposed under section 7B shall be—

S.NO

Profit on Debt

Rate of tax

(1)

(2)

(3)

1.

Where profit on debt does not exceed Rs.5,000,000

15%

2.

Where profit on debt exceeds Rs.5,000,000 but does not exceed Rs.25,000,000

17.5%

3.

Where profit on debt exceeds Rs.25,000,000 but does not exceed Rs. 36,000,000

20%

The tax rate is deducted under Section 7B of Income Tax Ordinance, 2001, under which:

Section 7B. Tax on profit on debt.—(1) Subject to this Ordinance, a tax shall be imposed, at the rate specified in Division IIIA of Part I of the First Schedule, on every person, other than a company, who receives a profit on debt from any person mentioned in clauses (a) to (d) of sub-section (1)of section 151.

(2) The tax imposed under sub-section (1) on a person, other than a company, who receives a profit on debt shall be computed by applying the relevant rate of tax to the gross amount of the profit on debt.

(3) This section shall not apply to a profit on debt that –

ISLAMABAD: Federal Board of Revenue (FBR) has updated income tax rate on dividend received from a company during tax year 2021 (July 01, 2020 – June 30, 2021).

The FBR issued Income Tax Ordinance, 2001 (updated up to June 30, 2020) incorporating amendments brought through Finance Act, 2020. The FBR updated following rate of dividend tax:

The rate of tax imposed under section 5 on dividend received from a company shall be-

(a) 7.5 percent in the case of dividends paid by Independent Power Producers where such dividend is a pass through item under an Implementation Agreement or Power Purchase Agreement or Energy Purchase Agreement and is required to be re-imbursed by Central Power Purchasing (CPPA-G) or its predecessor or successor entity.

(b) 15 percent in mutual funds and cases other than those mentioned in clauses (a) and (c).

(c) 25 percent in case of a person receiving dividend from a company where no tax payable by such company, due to exemption of income or carry forward of business losses under Part VIII of Chapter III or claim of tax credits under Part X of Chapter III.

Section 5 of Income Tax Ordinance, 2001 explains tax on dividends as:

Section 5. Tax on dividends.— (1) Subject to this Ordinance, a tax shall be imposed, at the rate specified in Division III of Part I of the First Schedule, on every person who receives a dividend from a company or treated as dividend under clause (19) of section 2.

(2) The tax imposed under sub-section (1) on a person who receives a dividend shall be computed by applying the relevant rate of tax to the gross amount of the dividend.

(3) This section shall not apply to a dividend that is exempt from tax under this Ordinance.

ISLAMABAD: Federal Board of Revenue (FBR) has updated rate of super tax to be applicable for tax year 2021 (July 01, 2020 – June 30, 2021).

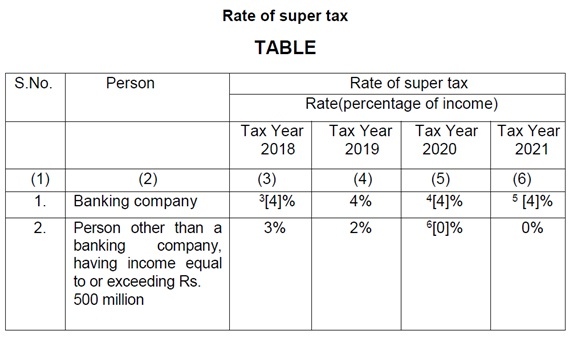

The FBR issued Income Tax Ordinance, 2001 after incorporating amendment brought through Finance Act, 2020. The FBR issued the following updated rate of super tax:

Provided that in case of a banking company, super tax for tax year 2019 shall be payable, on estimate basis, by thirtieth day of June, 2018.

Super tax was introduced through Finance Act, 2015 by inserting Section 4B to Income Tax Ordinance, 2001.

The section 4B is read as:

4B. Super tax for rehabilitation of temporarily displaced persons.― (1) A super tax shall be imposed for rehabilitation of temporarily displaced persons, for tax years 2015 and onwards, at the rates specified in Division IIA of Part I of the First Schedule, on income of every person specified in the said Division.

(2) For the purposes of this section, “income” shall be the sum of the following:—

(i) profit on debt, dividend, capital gains, brokerage and commission;

(ii) taxable income (other than brought forward depreciation and brought forward business losses) under section (9) of this Ordinance, if not included in clause (i);

(iii) imputable income as defined in clause (28A) of section 2 excluding amounts specified in clause (i); and

(iv) income computed, other than brought forward depreciation, brought forward amortization and brought forward business lossess under Fourth, Fifth, Seventh and Eighth Schedules.

(3) The super tax payable under sub-section (1) shall be paid, collected and deposited on the date and in the manner as specified in sub-section (1) of section 137 and all provisions of Chapter X of the Ordinance shall apply.

(4) Where the super tax is not paid by a person liable to pay it, the Commissioner shall by an order in writing, determine the super tax payable, and shall serve upon the person, a notice of demand specifying the super tax payable and within the time specified under section 137 of the Ordinance.

(5) Where the super tax is not paid by a person liable to pay it, the Commissioner shall recover the super tax payable under subsection (1) and the provisions of Part IV,X, XI and XII of Chapter X and Part I of Chapter XI of the Ordinance shall, so far as may be, apply to the collection of super tax as these apply to the collection of tax under the Ordinance.

(6) The Board may, by notification in the official Gazette, make rules for carrying out the purposes of this section.

ISLAMABAD: Federal Board of Revenue (FBR) has signed an agreement with Chartered Financial Analyst (CFA) Institute for initially 10 ‘Regulator Scholarships’ for FBR’s officers and officials, said a notification issued on Thursday.

The CFA Institute, an America-based Organization, is a global association of investment professionals. The organization offers Certifications for Chartered Financial Analyst (CFA), Investment Performance Measurement (CIPM) and Investment Foundations Certificate. Currently, CFA Institute offices are located in New York City, London, Hong Kong, Mumbai, Toronto, and Charlottesville, Virginia, USA.

The CFA Program is a professional credential offered internationally by the CFA Institute to investment and financial professionals and is recognized as a ‘Gold Standard’ qualification in investment management. The program covers a broad range of topics relating to investment management, financial analysis, quantitative analysis, equities, fixed income and derivatives, and provides generalist knowledge of other areas of finance combined with real world skills and case studies. A candidate who successfully completes the program and meets other professional requirement is awarded the “CFA Charter” and becomes a CFA.

Under the Scholarship, Program Enrollment Fee is waived off and exams registration fee is reduced to USD 350 compared to standard registration fee of USD 1,000.

FBR’s workforce needs to equip itself with the modern skills and techniques involved in investment management, financial analysis and all other relevant areas to better understand the intricacies involved in financial management and income generated through various investment vehicles. Therefore, FBR’s officers/officials are encouraged to benefit from the scholarship programme to leverage the ongoing professional learning and industry network that CFA Institute and CFA Society Pakistan can provide.

Interested candidates must apply and be awarded the scholarship before registering for an exam, so that scholarship discount will be applied at the time of payment. The process is:

i) Candidates set up a CFA account and apply through the online system for a regulator scholarship.

ii) Regulator approvers log in to the system and award, or decline the scholarship application.

iii) If awarded, the candidate is notified by the CFA Institute. The scholarship is then applied to their CFA account, so that when they register for an exam the discount is applied at time of payment. All further activity is directly between the candidate and the CFA Institute.

iv) If declined, the candidate is notified by the CFA Institute and may choose to apply for the exam as normal without the discount.

The selection of eligible candidates would be done by International Taxes, FBR. After having gone through the selection exercise, the names of the selected candidates will be forwarded to the CFA Institute for the grant of scholarship.