The Pakistan Business Council (PBC) has expressed its dissatisfaction with the imposition of super tax on corporate profits, describing it as a penalty on the documented sector.

(more…)Tag: super tax

-

Supreme Court orders taxpayers to pay half of super tax

ISLAMABAD: Supreme Court of Pakistan (SCP) on Monday ordered the taxpayers to pay half of the super tax within seven days, according to a Tweet by the Federal Board of Revenue (FBRP).

(more…) -

What is super tax and who are required to pay?

Super tax is a special levy that is imposed on certain classes of taxpayers on their income in Pakistan. The collection of super tax has been made under Income Tax Ordinance, 2001.

Through Section 4B of the Income Tax Ordinance, 2001, super tax for rehabilitation of temporarily displaced persons was introduced through Finance Act, 2015. The tax was imposed till Tax Year 2022.

Another Section 4C of the Income Tax Ordinance, 2001, super tax on high earnings persons was introduced through Finance Act, 2022.

READ MORE: What income is taxable in Pakistan?

Following are the text of both the sections as per the Income Tax Ordinance, 2001 updated up to June 30, 2022, issued by the Federal Board of Revenue (FBR).

Section 4B. Super tax for rehabilitation of temporarily displaced persons.― (1) A super tax shall be imposed for rehabilitation of temporarily displaced persons, for tax years 2015 and onwards, at the rates specified in Division IIA of Part I of the First Schedule, on income of every person specified in the said Division.

(2) For the purposes of this section, “income” shall be the sum of the following:—

(i) profit on debt, dividend, capital gains, brokerage and commission;

(ii) taxable income(other than brought forward depreciation and brought forward business losses) under section (9) of this Ordinance, if not included in clause (i);

READ MORE: FBR, SBP discuss stuck-up consignments, LC opening

(iii) imputable income as defined in clause (28A) of section 2 excluding amounts specified in clause (i); and

(iv) income computed, other than brought forward depreciation, brought forward amortization and brought forward business lossess under Fourth, Fifth, Seventh and Eighth Schedules.

(3) The super tax payable under sub-section (1) shall be paid, collected and deposited on the date and in the manner as specified in sub-section (1) of section 137 and all provisions of Chapter X of the Ordinance shall apply.

(4) Where the super tax is not paid by a person liable to pay it, the Commissioner shall by an order in writing, determine the super tax payable, and shall serve upon the person, a notice of demand specifying the super tax payable and within the time specified under section 137 of the Ordinance.

READ MORE: World Bank satisfied with progress of Pakistan Raises Revenue Program

(5) Where the super tax is not paid by a person liable to pay it, the Commissioner shall recover the super tax payable under subsection (1) and the provisions of Part IV,X, XI and XII of Chapter X and Part I of Chapter XI of the Ordinance shall, so far as may be, apply to the collection of super tax as these apply to the collection of tax under the Ordinance.

(6) The Board may, by notification in the official Gazette, make rules for carrying out the purposes of this section.

4C. Super tax on high earning persons.― (1) A super tax shall be imposed for tax year 2022 and onwards at the rates specified in Division IIB of Part I of the First Schedule, on income of every person:

Provided that this section shall not apply to a banking company for tax year 2022.

(2) For the purposes of this section, “income” shall be the sum of the following:—

(i) profit on debt, dividend, capital gains, brokerage and commission;

(ii) taxable income (other than brought forward depreciation and brought forward business losses) under section 9 of the Ordinance, excluding amounts specified in clause (i);

(iii) imputable income as defined in clause (28A) of section 2 excluding amounts specified in clause (i); and

(iv) income computed, other than brought forward depreciation, brought forward amortization and brought forward business losses under Fourth, Fifth and Seventh Schedules.

READ MORE: FBR Member PR holds meetings to create return filing awareness

(3) The tax payable under sub-section (1) shall be paid, collected and deposited on the date and in the manner as specified in sub-section (1) of section 137 and all provisions of Chapter X of the Ordinance shall apply.

(4) Where the tax is not paid by a person liable to pay it, the Commissioner shall by an order in writing, determine the tax payable, and shall serve upon the person, a notice of demand specifying the tax payable and within the time specified under section 137 of the Ordinance.

(5) Where the tax is not paid by a person liable to pay it, the Commissioner shall recover the tax payable under sub-section (1) and the provisions of Part IV, X, XI and XII of Chapter X and Part I of Chapter XI of the Ordinance shall, so far as may be, apply to the collection of tax as these apply to the collection of tax under the Ordinance.

(6) The Board may, by notification in the official Gazette, make rules for carrying out the purposes of this section.

-

Super tax imposed only for one year: Miftah

KARACHI: Finance Minister Dr. Miftah Ismail has said that super tax at the rate of 10 per cent has been imposed only for one year.

The minister said: “Fiscal discipline will be strictly followed and all additional expenditures will be fully funded by tax measures. The 10 percent Super Tax is only imposed for one year while alternative revenue streams are developed. ADR linked tax on banks will not be imposed retrospectively and tax revenues from the retail sector are expected to be significantly more compared to last year.”

READ MORE: Pakistan welcomes UAE $1 billion investment

He expressed these views in the meeting hosted by Pakistan Stock Exchange (PSX), said the statement.

Dr. Miftah Ismail clarified that, “Macro economic stability was forthcoming with the IMF programme resuming before end of August as all conditionalities had been met.

Furthermore, the balance of payments position is now well under control. With increased hydel power, lower energy demand and lower oil prices, Pakistan may even have balance of payments surplus in coming months.

Chairperson PSX, Dr. Shamshad Akhtar; Chairman SECP, Aamir Khan; MD & CEO PSX, Farrukh H. Khan; Chairman FBR, Asim Ahmad; Deputy Governor SBP, Dr. Inayat Hussain; Special Secretary Finance, Awais Manzoor, and key stakeholders including Chairman Arif Habib Group, Arif Habib; Chairman Pakistan Stock Brokers Association (PSBA) & AKD Group, Aqeel Karim Dhedhi; CEO Bank Alfalah Limited, Atif Bajwa; CEO NBP Funds, Dr. Amjad Waheed; Director Arif Habib Corporation, Nasim Beg, and CEO Pakistan Business Council (PBC), Ehsan Malik, participated.

READ MORE: Pakistan’s foreign reserves dip to $14.21 billion

The meeting involved discussion on proposals presented by PSX to the Finance Minister for the sustainable development of the capital markets.

This follow-up meeting came on the heels of the visit of the Finance Minister to PSX on Friday (August 5).

The MD PSX welcomed the finance minister and other participants and thanked them for their presence at this follow-up meeting.

The MD PSX re-emphasized that the situation in the capital markets needed to be addressed on a war-footing.

The key points addressed at the meeting included matters related to Pakistan’s macro-economy, capital markets, taxation and non-tax measures.

READ MORE: Pakistan’s trade deficit narrows by 18% in July 2022

In terms of the macroeconomic situation prevailing in the country, the participants emphasized that government’s funding should be strong and taxation measures should be equitable.

Movements in PKR/USD exchange rate have been too volatile and changes to this effect should be gradual.

With regard to the interest rates, it was pointed out that interest rates in almost all countries of the world are negative and that this must be taken into account in context of interest rates in Pakistan.

With respect to the capital markets, it was discussed in the meeting that urgent actions be taken to mitigate the impact of macro developments for sustained and secular growth of the capital markets.

As perhaps the largest stakeholder in the market, the government will benefit directly by developing better funding alternatives, improved documentation and higher tax revenue, as well as avail the broader benefits that accrue to an economy on account of having developed capital markets.

It was emphasized that the two biggest obstacles to capital markets growth are tax incentives given to other asset classes and KYC requirements in the stock market, which were not consistently applied to other asset classes.

READ MORE: Pakistan inflation hits 14-year high at 25% in July

These obstacles are resulting in an AML and tax driven distortion amongst asset classes which is detrimental to efficient allocation of scarce resources in Pakistan; hence creating challenges on both demand and supply sides for the capital markets.

In terms of taxation, the participants of the meeting pointed out that even though the stock market is undoubtedly one of the most documented sectors of the economy, however, income of listed companies is subject to double tax, at the company level and later on dividends distribution level as well, whereas unincorporated businesses are subject to substantially lower taxes. It was emphasized that this inequity in taxation is discouraging corporatisation and documentation.

The points made to encourage corporatisation and documentation included tax rate for unlisted companies and AOPs be logically higher than for listed companies, restoration of tax credit for newly listed companies as the immediate revenue impact is very small.

In the medium term this will be a revenue positive measure since FBR will collect both CGT and higher income tax from both the listed companies and other companies in the supply chain of the listed companies, provide a small tax rebate to any listed company that pays more than 50% of profits as dividends, reinstate exemption on inter-corporate dividend under clause 103c for group relief which will significantly improve capital formation and investments, and grandfather tax position of companies at the time of new listing on PSX, particularly for smaller companies listing on the GEM Board of PSX.

A key concern expressed at the meeting was the treatment of CGT. The Finance Bill 2022 addressed this issue through introduction of reduced rates based on holding period.

However, the final Amended Finance Bill 2022 has again created tax disparity between securities and immovable properties. This was termed unfair and against the stated policy of GoP.

In terms of non-tax measures, it was emphasized that SOEs like State Life, DFIs like Pak Kuwait, PPP, and CPEC projects be encouraged to list and raise debt from the capital market. This will allow the GoP to release their equity and reinvest it in new projects, while growing the size of the market, a key matric to be included in the MSCI Emerging Markets Index.

Additionally, it was pointed out that Direct Listing procedure developed by SECP and PSX can be used to achieve this without any significant sale of shares by GoP.

The participants in the meeting further emphasized that all measures/ schemes introduced by GoP, MoF, FBR and SBP should be available on better terms for listed companies such as concessional financing schemes for SMEs, that GoP use the capital markets for further Sukuk and debt issues for itself and other GoP controlled entities, that the term ‘Advances’ for the purpose of calculating ADR under the Income Tax Ordinance, 2001 must include investment in all kinds of Corporate Sukuks/ TFCs, that investment limit for small retail investors, with easier AML requirements in Sahulat Accounts be increased to Rs.2.5 million with SECP fully clarifying AML requirements for Sahulat Accounts, that reforms in NSS are extremely important to eliminate distortions in the financial sector and to create significant savings for the GoP.

The Finance Minsiter was highly receptive to all the points discussed. In particular, he asked the FBR to immediately review any discrepancies in the CGT regime and the issue of tax credit for newly listed companies. He asked SECP to review the investment limit and AML requirements for Sahulat Accounts. He also directed the MoF to review listing of DFIs, procedure for issuance of debt/ Sukuks in the capital markets and interest rate setting of NSS instruments.

Infact, for a thorough review of all the above matters, the Finance Minister set up three committees. The first committee was set up to share the perspective of the private sector with SBP and the MPC on interest rates, the second one was set up to coordinate with PBC and PSX on all the tax issues and the third committee was set up to coordinate the review of listing of DFIs, debt & Sukuk issuance, reform of NSS and explore development of a market for exchange rate forward dealing which all market participants can access. In the first committee, the Deputy Governor SBP, Dr. Inayat Hussain will coordinate with representatives of PSX and PBC. In the second committee, Member Tax Policy, Mr. Afaque Qureshi will coordinate with PBC and PSX on all tax issues whereas in the third committee, Special Secretary Finance, Mr. Awais Manzoor will coordinate along with Mr. Nasim Beg from the private sector.

The Finance Minister further committed to review progress and meet with the stakeholders again within two weeks. On behalf of all stakeholders, PSX thanked the Finance Minister and his team on the positive and constructive discussion, expressing confidence in materialisation of concrete actions in the next two weeks.

-

Super tax to hammer auto business in Pakistan: Honda Atlas

KARACHI: Honda Atlas Cars (Pakistan) Limited on Thursday said that super tax to hammer the already thin margins of the auto business in the country.

The company in its detailed financial report said: “The imposition of Super Tax will further hammer the already thin margins of auto business.”

The company said that the automobile industry is considered as one of the key sectors for rapid transformation of the economy.

READ MORE: Suzuki Motors warns plant shutdown in Pakistan

Likewise, the automobile industry of Pakistan epitomizes considerable growth, capacity building and technological prowess.

“The current state of auto sector, however, has matured differently through the quarter under review. Adverse USD/PKR exchange rate parity and global supply glitches continue to undermine the Industry’s potential throughout,” it said.

Moreover, the fiscal measures adopted by the State Bank of Pakistan (SBP) for the management of foreign reserves has unavoidably impacted the import and production schedules lately.

READ MORE: Indus Motors rebuts plant shutdown reports

Rupee devaluation has approached an alarming level under the vague economic and political direction; further aggravating the situation.

“Resultantly, the car customers are facing delays in delivery, hikes in prices and temporary non- availability of some car variants,” the company said.

Honda Atlas Cars said during the period under review, the sales and production of the four-wheeler segment have not been up to the Industry’s expectation owing to curbed auto lending, escalating inflation and soaring fuel prices.

The overall industry production for the three months ended June 2022 remained 71,745 units in comparison with 53,915 units a year ago while car sales were observed at 73,815 units against 46,679 units during the same period.

READ MORE: Toyota Indus Motors offers 100% refunds on booking cancellation

The company produced 9,324 units against 7,826 units and sold 9,446 units as compared to 7,598 units in the same period of last financial year.

The recently approved Federal Budget 2022-2023 also poses tough times ahead for the auto industry. Amid negotiations with International Monetary Fund (IMF), to release the bailout package, the Government had to enforce stringent stabilization measures. Accordingly, the purchase of automobiles with engine capacity exceeding 1300CC has now been subject to 1 per cent of Capital Value Tax (CVT).

The advance tax on vehicles with engine capacity above 1600CC has also been significantly increased.

These revenue measures by the Government will further burden the customers, which may affect the Industry’s sales volume.

READ MORE: Toyota lowers July production in Japan

The imposition of Super Tax will further hammer the already thin margins of auto business.

The auto industry may experience a further slowdown in anticipation of price revision and rising interest rates.

Ranging from raw material sourcing to management of stable commodity pricing and customary lead time, the automobile industry is currently in the midst of multiple challenges.

During the quarter, the OEMs have managed to avoid potential shut down of production due to relatively higher stock levels. This led to improved financial results for the 1st quarter of the new financial year.

During the three months ended June 30, 2022, the Company achieved net sales revenue of Rs 30,246 million as compared to Rs 21,765 million in the corresponding period last year.

Higher production volumes with better overhead absorption helped to generate gross profit of Rs 1,915 million against Rs 1,595 million, a year ago. The selling and administrative expenses were increased to Rs 575 million against Rs 363 million.

Other income improved to Rs 526 million against Rs 335 million owing to customers’ confidence on the Company’s products and better funds management; benefited by increased interest rates.

The Company posted Rs 1,094 million as profit before tax in comparison to Rs 1,364 million. After statutory tax adjustments, including super tax provision, the net profit for the three month period ended June 30, 2022 came out Rs 658 million as compared to Rs 928 million of the corresponding period last year.

The earning per share remained Rs 4.61 against Rs 6.50 for three months of the last year.

-

Super tax to apply for Tax Year 2022 and onwards: FBR

ISLAMABAD: The Federal Board of Revenue (FBR) on Thursday said that super tax will be applicable for tax year 2022 and onwards.

The FBR issued Income Tax Circular No. 15 of 2022/2023 to explain important amendments made to Income Tax Ordinance, 2001 through Finance Act, 2022.

READ MORE: Pakistan enhances income tax rates for banks

The FBR said that a new section 4C to Income Tax Ordinance, 2001 has been introduced through Finance Act, 2022 and this section will apply for tax year 2022 and onwards.

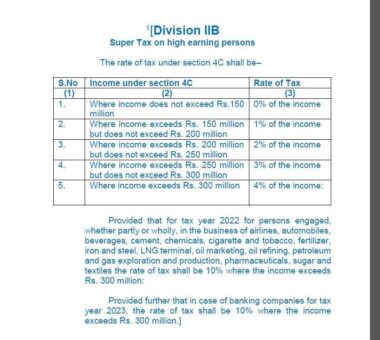

Except for the persons whose income as envisaged in this section is below Rs150 million, all other persons including those assessed under Fourth, Fifth and Seventh Schedules to the Ordinance are liable to pay super tax on graduated rates ranging from 1% to 4% based on graduated income slabs provided in Division JIB of Part I of First Schedule given as under:

READ MORE: Declaring beneficial owner made mandatory for companies, AOPs

S. No. Income under Section 4C Rate of Tax 1. Where income does not exceed Rs150 million 0% of the income 2. Where income exceeds Rs150 million 1% of the income but does not exceed Rs200 million 1% of the income 3. Where income exceeds Rs200 million 2% of the income but does not exceed Rs250 million 2% of the income 4. Where income exceeds Rs250 million but does not exceed Rs300 million 3% of the income 5. Where income exceeds Rs300 million 4% of the income However, for tax year 2022 the rate of super tax under this section will be 10% instead of 4%, where the income of the persons engaged, partly or wholly, in business of airlines, automobiles, beverages, cement, chemicals, cigarette & tobacco, fertilizer, iron & steel, LNG terminal, oil marketing, oil refining, petroleum & gas exploration and production, pharmaceuticals, sugar and textiles exceeds Rs.300 million. For tax year 2023, this super tax on income of banking companies will be 10% if the income for the year exceeds Rs. 300 million.

READ MORE: Pakistan reintroduces capital value tax on motor vehicles

For the purposes of this section, the income will be the sum of the following:

(i) Profit on debt, dividend, capital gains, brokerage, and commission;

(ii) Taxable income (other than brought forward depreciation and brought forward business losses) under section 9 of the Ordinance, excluding amounts specified in (i) above;

(iii) Imputable income as defined in clause (28A) of section 2 excluding amounts specified in clause (i) above; and

(iv) Income computed, other than brought forward depreciation, brought forward amortization and brought forward business losses under Fourth, Fifth and Seventh Schedule.

READ MORE: Customs duty exemption, concession granted

Super tax payable under this section will be paid on the date and manner as specified in under section 137(1) of the Ordinance.

In case of default by the person liable to pay super tax under this section, Commissioner through an order in writing will determine the liability of the person and proceed to recover the same under applicable provisions of the Ordinance, the FBR added.

-

FPCCI denounces super tax imposition

KARACHI: Federation of Pakistan Chambers of Commerce and Industry (FPCCI) has denounced the imposition of super tax by the government to generate additional revenue.

(more…) -

Pakistan slaps super tax on industries, individuals

ISLAMABAD: Pakistan on Friday imposed a 10 per cent super tax on earnings of certain industrial sectors and on income of high net worth individuals.

Prime Minister Shehbaz Sharif announced to impose the 10 percent super tax on over 12 large industries and also on affluent persons with more than Rs 150 million annual income with a rate up to four percent.

Addressing the members of his economic team, he said the imposed taxes would be the “first step towards the country’s financial self-reliance”.

READ MORE: Key tax measures taken through Finance Bill 2022

The prime minister said the 10 percent tax aimed at poverty alleviation would be imposed on industries and sectors including cement, fertilizers, steel, sugar, textile, oil and gas, LNG terminals, banking sector, cigarette, chemicals and beverages.

He said the individuals earning over Rs 150 million a year would pay one percent tax; those earning Rs 200 million will pay two percent, those over Rs 250 million income to pay three percent and the ones earning above Rs 300 million will pay four percent tax.

The prime minister said he had formed teams to boost tax collection with the help of organs of State institutions and through digital means.

READ MORE: FPCCI identifies tax anomalies in budget 2022-2023

He said the step would help the country attain economic stability and push it out of the shakles of loans.

PM Sharif pointed out that every year, an amount of around Rs 2,000 billion in the country was misappropriated through tax evasion.

He mentioned that 60 percent of the formal sector was paying taxes, however the rest of 40 percent economy needed to be brought into tax net.

He said the collected tax would be diverted towards the projects of health, education, skilled training and information technology.

For the first time in country’s history, he said, a budget had been presented to provide relief to common man, orphans, widows and poor.

READ MORE: Pakistan announces massive tax reduction for salaried persons

The prime minister hoped that with hard work and faith in Allah Almighty, the things would ease up.

The measures taken in the budget will enable the poor overcome their financial challenges, he added.

PM Sharif said the history was evident that the poor always sacrificed while facing challenges, but now it was the moral obligation upon the affluent to come forward and contribute.

He expressed confidence that the measures would take Pakistan forward on the path of prosperity, progress and economic stability.

-

Section 4B of Income Tax Ordinance, 2001: super tax

ISLAMABAD: The Section 4B of the Income Tax Ordinance, 2001 deals with super tax for rehabilitation of temporarily displaced persons. The Federal Board of Revenue (FBR) issued the updated Income Tax Ordinance, 2001.

(more…) -

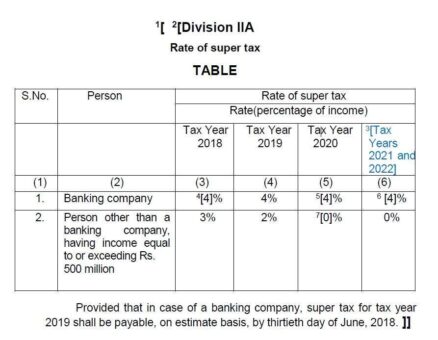

Super tax permanently imposed on banking companies

ISLAMABAD: The levy of super tax has been permanently imposed on banking companies as it was expiring in the tax year 2021.

Sources in the Federal Board of Revenue (FBR) said that the super tax was only imposed on banking companies while the other taxpayers were exempted from tax year 2020.

The sources said that the Finance Bill 2021 had proposed to continue the levy of super tax at 4 percent on banking companies beyond Tax Year 2021 and onwards.

The government imposed the super tax through Finance Act, 2015 for one year, which was later extended for subsequent years, by inserting Section 4B to the Income Tax Ordinance, 2001.

According to Section 4B:

Super tax for rehabilitation of temporarily displaced persons.― (1) A super tax shall be imposed for rehabilitation of temporarily displaced persons, for tax years 2015 and onwards, at the rates specified in Division IIA of Part I of the First Schedule, on income of every person specified in the said Division.

(2) For the purposes of this section, “income” shall be the sum of the following:—

(i) profit on debt, dividend, capital gains, brokerage and commission;

(ii) taxable income (other than brought forward depreciation and brought forward business losses) under section (9) of this Ordinance, if not included in clause (i);

(iii) imputable income as defined in clause (28A) of section 2 excluding amounts specified in clause (i); and

(iv) income computed, other than brought forward depreciation, brought forward amortization and brought forward business lossess under Fourth, Fifth, Seventh and Eighth Schedules.

(3) The super tax payable under sub-section (1) shall be paid, collected and deposited on the date and in the manner as specified in sub-section (1) of section 137 and all provisions of Chapter X of the Ordinance shall apply.

(4) Where the super tax is not paid by a person liable to pay it, the Commissioner shall by an order in writing, determine the super tax payable, and shall serve upon the person, a notice of demand specifying the super tax payable and within the time specified under section 137 of the Ordinance.

(5) Where the super tax is not paid by a person liable to pay it, the Commissioner shall recover the super tax payable under subsection (1) and the provisions of Part IV,X, XI and XII of Chapter X and Part I of Chapter XI of the Ordinance shall, so far as may be, apply to the collection of super tax as these apply to the collection of tax under the Ordinance.

(6) The Board may, by notification in the official Gazette, make rules for carrying out the purposes of this section.